BIMCOs Shipping Market Overview & Outlook – June 2021. Focus: dry bulk and macroeconomics

Macroeconomics: pandemic disruption hits supply chains as multi-paced recovery takes hold

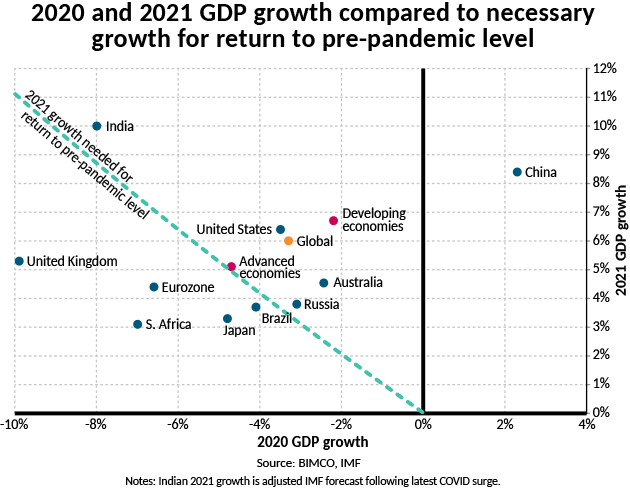

Despite diverging pandemic paths in the world, global growth is forecast to reach 6% this year, according to the International Monetary Fund, following a 3.3% contraction last year. There are, however, still plenty of downside risks, especially as parts of the world are facing their worst coronavirus outbreaks to date and the prospect of a large part of the global population being vaccinated is still a long way off.

Even in countries that seem to have the worst of the pandemic behind them, growth this year is expected to vary. China and the US are expected to forge ahead, solidifying their position as the top two global economies, whereas the EU, Japan and the UK are lagging behind and need at least another year to return to pre-pandemic levels.

With the global recovery picking up steam as vaccines are rolled out widely across the developed world, manufacturing activity is picking up, especially in developed economies where it dropped last year, unlike in China where it drove the recovery.

Despite April seeing the highest number of confirmed COVID-19 cases so far, the global manufacturing PMI reached its highest level since April 2010, at 55.8, the tenth month of expansion. The higher PMI is a result of not only rising ouput and new orders – though both of these have been strong (55.7 and 56.7, respectively) – but also longer supplier delivery times and higher input prices as manufacturers struggle to secure all the raw materials they need to keep up with their orderbooks.

The strength of consumer demand for manufactured goods and the unpredictability of the past year has left supply chains under more pressure now than at any other point in this pandemic, as securing the needed inputs has become an increasing challenge in many industries, with delays and temporary factory closures still being announced worldwide.

In the attached report you will find focus sections for Asia, US and Europe.

Outlook for macroeconomics

With the pandemic still raging, the number of daily new confirmed cases and deaths rising, and a geographically very uneven vaccine distribution, the post pandemic world is still some way off. However, despite all the risks the current situation still presents, the richest economies in the world are lifting restrictions, which – if they avoid new surges – will boost their economies.

Although services are picking up in countries where the vaccine roll-out is going well, goods will continue to drive global economic growth. The World Trade Organization forecasts that merchandise trade will grow by 8.0% in 2021 (after a 5.3% drop in 2020), with container and dry bulk shipping both seeing record high volumes so far this year. As long as travel restrictions and social distancing measures remain in place, however, global oil demand, and thereby demand for tanker shipping, will remain far from record levels.

The delays in supply chains that are affecting production around the world will also continue to cause problems for many months to come, as manufacturers scramble to piece together the components needed for their production lines. While a knee-jerk reaction for some will be to look at options for relocating production and increasing protectionism, the solution to a global problem will have to happen on a global scale. Protectionist measures will only complicate the issue.

As The Economist puts it: “Globalisation is the work of decades. Do not let it run aground”.

Dry bulk shipping: record-breaking start to year drives earnings to decade highs

Demand drivers and freight rates

The first four months of 2021 have been record-breaking in volume terms, with demand reaching 1.69 billion tonnes – the highest-ever start to a year. Volumes are up 6.1% compared with the same period in 2020, and only slightly down from the 1.72 billion tonnes in the final four months of 2020. Strong starts to the year for the high-volume commodities of iron ore and coal – thanks to infrastructure-heavy stimulus in some parts of the world – as well as plenty of agricultural exports, have all contributed to the record-breaking start, with strong volumes clearly reflected in dry bulk earnings.

So far, Capesize earnings are on track for the best month of May since 2010, with a daily average of USD 36,536 per day, more than 9 times that of May 2020. The current strength of the market is only underlined by comparing current earnings to peak seasons in past years. The last time average earnings in Q4 were above even USD 25,000 per day was in 2013, and to get above May’s average so far, you have to go back to Q2 2010.

The rest of the market is also delivering strong profits to owners and operators, with Panamax earnings standing at USD 24,903 per day and Supramaxes USD 27,43 per day on 26 May. Even for a 38,000 DWT Handysize ship, earnings are above USD 24,000 per day.

Just as freight rates are up for all ship sizes, the appetite for cargo transport has increased across the board. Supramaxes are the biggest winners, with demand for these soaring by 10.6% in the first four months of this year, compared with 2020. Capesize demand rose by 6.0%, while Panamax edged up 1.5%. Demand for Handysize ships grew the least compared to its pre-pandemic level, up just 0.1% from the first four months of 2019, despite 7.3% growth from the start of 2020.

Focus section on fleet news is found in the attached report.

Outlook for dry bulk shipping

So far this year, coal demand has developed differently across the shipping segments. Almost half of all seaborne coal trade happens on Panamax ships where volumes in the first four months of this year fell by 3.6%; meanwhile, coal demand on Capesize ships grew by 6.5% (source: Oceanbolt).

Demand for coal is increasingly coming under scrutiny, especially following US President Joe Biden’s Climate Summit and in the lead up to the COP26 climate summit in Glasgow, which is expected to be held in November. Despite this, concrete targets were few and far between when it came to the largest coal consumers.

At the Biden Climate Summit, China announced its coal consumption would continue to grow over the next five years, albeit at a more limited rate. It then committed to peak its coal consumption in the next five-year plan that runs between 2026 and 2030. With imports making up only a small part of total consumption, given China’s large domestic production, it will be up to the Chinese to decide which source they want to cut down on first. Even if imports are the first to go, a sudden drop is not just round the corner.

Also included in China’s new five-year plan is an increased focus on technology and high-value manufacturing. This indicates a move away from the more traditional construction and heavy industry sectors, potentially lowering demand for some Chinese dry bulk goods over the next few years.

Muddying the water is the deteriorating relationship between China and Australia, although the iron ore trade between the two nations looks to be protected as both are highly dependent on it.

India, the second-largest coal importer, offered even fewer targets on its path to decarbonisation. Coal and lignite feeds 54.7% of the country’s current installed power generation capacity. Other than a pledge to increase its renewable energy capacity by 450 gigawatts by 2030, there was little talk of limiting coal consumption or imports at the Biden summit.

Despite the current strength of the dry bulk market, fundamentally little has changed, with high demand primarily being driven by short-term factors linked to pandemic-related stimulus spending and stockpiling. This means that, even though volumes are currently strong and the orderbook relatively low, BIMCO is not holding its breath for the next supercycle to begin.

Whatever happens in the longer run, the strong start to this year has padded dry bulk owners’ and operators’ bottom lines, and with continued strong demand for many of the major dry bulk goods, this year looks set to be one to remember.