- There have been sharp declines in the US stocks, bonds and the dollar since President Trump’s ‘Liberation Day.’

- There are now questions whether the US dollar’s role as the world’s reserve currency is under threat.

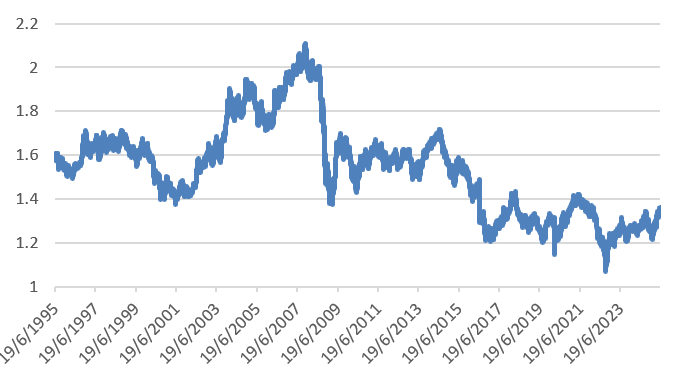

- Dollar weakness has continued over the past month – recent performance of dollar against sterling is the worst in 30 years.

- A look at whether there are any real alternatives.

Robert Farago, head of strategic asset allocation, Hargreaves Lansdown:

“The recent plunge in the value of the US dollar was its worst performance in 30 years. The parallel decline in stocks, bonds and the currency is something we associate with emerging market crises: when investors lose confidence in a country and sell everything. It wasn’t always like this. In a typical crisis, the credit window – companies’ ability to borrow – goes from wide open to slammed shut in an instant. This leaves borrowers scrambling for funds – and much of that funding around the world is in dollars. This helps push up the value of the US dollar against other currencies. The dollar also typically gains when the US economy is booming and demand for borrowing is strong. Other currencies advance against the dollar in a Goldilocks economy: not too hot, not too cold. This creates a ‘dollar smile’: rising when the economy is either weak or strong but falling in between. Today, that smile has turned to a frown.

The alternatives

Changes in the world’s dominant currency are rare. The Spanish ‘pieces of eight’ underpinned the global financial system in the sixteenth century, followed by the Dutch guilder a century later. The pound sterling reigned supreme from the end of the Napoleonic War until the baton passed to the dollar between World War I and World War II. The US economy surpassed the UK economy – and its Empire – years before the dollar outstripped the pound in financing global trade. These century-long eras put the last few months of policy turmoil into context.

Which currency could replace the US dollar? Larry Summers, the former US Treasury Secretary summed up the challenge: ‘Europe is a museum, Japan is a nursing home, China is a jail, and Bitcoin is an experiment.’ No other currency offers the same liquidity in high quality government bonds to match the US. Europe remains an unfinished union: reluctant to issue joint bonds at the scale needed. China maintains capital controls that mean the renminbi is a tiny proportion of the reserves of the world’s central banks.

Gold is a viable store of value. But it too bulky to be practical for payments in cross-border trade.

Tip-toeing towards a multi-currency world

None of this means that the dollar’s role cannot shrink. Indeed, the dollar’s share of global foreign exchange reserves has fallen from around 70% to under 60% over the last 25 years.

This decline has been offset by a growing use of currencies from small, well-managed economies: Switzerland, Australia, Canada, New Zealand, Singapore, South Korea, Denmark and Norway. Central bank reserve managers are diversifying geographically – in the same way that we encourage investors to do. Emerging markets are building direct ties that cut out the currencies of the developed world. Brazil plans to issue ‘Panda Bonds’ – debt issued in Chinese renminbi – later this year.

The role of the US dollar seems secure. But the new administration is pursuing policies that could undermine this stability. Trump’s chief economist, Stephen Miran, has proposed a Mar-a-Lago accord that threatens to forcibly convert foreign holdings of US government bonds into hundred-year bonds paying low interest rates. We would expect this to have a dramatic negative effect on markets. This makes it unlikely to occur. But, after the events of the last few months, it is hard to be confident when predicting the direction of US policy. We expect the US dollar to maintain its dominant role among global currencies. But it’s likely there will be a gradual shift towards a more multi-polar world over the next decade. And investors cannot ignore the risk that policy shocks accelerate this trend.”

Dollar vs sterling performance over last 30 years