Q2 2025

SHIPPING MARKET ANALYSIS

Introduction

I am pleased to welcome you to the Q2 2025 edition of the Shipping Market Analysis. This quarter was marked by increasing divergence between individual markets, with volatility driven by ongoing geopolitical uncertainties, limited available shipyard space and critical regulatory milestones. Tanker markets maintained their momentum, supported by strong demand and limited fleet growth, while dry bulk freight showed mixed signals due to sluggish freight rates and fleet aging. Container markets have seen transient increases due to disruptions in trade flows but remain structurally fragile. At the same time, gas markets have gradually recovered, as long-term expectations boost investment in dual-fuel vessels.

Building on the momentum of Q1, our Sustainability Unit continues to monitor the industry’s transformational developments. The path towards decarbonisation has been further strengthened this quarter, with a wave of innovations in fuel technologies, carbon capture systems, wind-assisted propulsion and digital tools. Regulatory pressure is intensifying, especially with the entry into force of the Hong Kong Convention and the expansion of the Zones Emissions Control, highlighting the need for strategic fleet planning and compliance readiness.

This exhibition is the result of the collective work of our team at the Department of Port and Shipping Management of the National and Kapodistrian University of Athens.

Head of Scientific Research:

Dr. Michael Tsatsaronis, Assistant Professor, Department of Port Management and Shipping, National and Kapodistrian University of Athens

Research Team:

Dimopoulos Argyris, Markopoulioti Panagiota, Mania Amalia, Vasileiadou Savvina, Zifkou Kalliopi, Doumani Panagiota, Katsavos George, Vitzilaiou Anastasia, Zacharopoulou Efthimia, Stratikopoulos Dimitris, Karasavvidis Theocharis, Skouli Maria Aikaterini, Spyraki Sofia, Karapanagou Angeliki, Gaki Margarita, Polonyfi Stavriani, Gkorila Martha.

For inquiries or cooperation, please contact:

TANKER MARKET

FREIGHT MARKET

In April 2025, the global tanker market continued to experience significant shifts, shaped by evolving regulatory, economic, and geopolitical dynamics. A recent proposal by the U.S. Trade Representative (USTR) to tighten trade measures has prompted shipping companies to reassess vessel deployment strategies and routing. Simultaneously, the EU embargo on Russian petroleum products and the G7 price cap have redirected Russian oil exports toward Asia—particularly China and India—spurring demand for long-haul VLCC shipments.

As Europe turns to alternative suppliers like Saudi Arabia, Russian diesel flows are increasingly being rerouted toward North Africa and the Mediterranean, primarily via MR1 tankers. These adjustments have reshaped global oil trade patterns and contributed to higher tonne-mile demand. However, overall tanker demand has begun to soften due to persistent trade tensions, slowing global economic growth, and the accelerating transition to electric vehicles—especially in China—which is reducing oil consumption and placing downward pressure on freight rates.

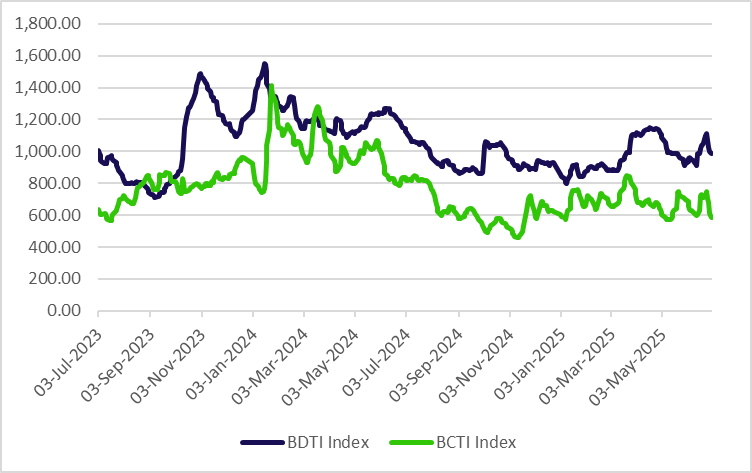

Graph 1: Baltic Dirty Tanker and Clean Tanker Index

By May 2025, the tanker market showed tentative signs of recovery, despite continued geopolitical and economic uncertainty. A key potential catalyst was the ongoing U.S.–Iran negotiations, which, if successful, could ease sanctions and unlock substantial volumes of Iranian oil exports—offering a near-term boost to tanker demand but also introducing volatility.

Shifting global trade flows—driven by Asia’s growing energy needs and a rise in long-haul shipments—continued to support tanker utilization and freight rates, although weaker-than-expected Chinese imports and its policy shift toward energy efficiency and renewables have slightly dampened growth on specific routes.

Meanwhile, the aging global tanker fleet remains a pressing concern. Over 17% of vessels are now older than 21 years—a share expected to nearly double by 2029—leading to higher maintenance costs and compliance challenges amid stricter emissions regulations. This has spurred investment in fleet renewal, with Greek shipping companies particularly active in securing financing for new, eco-friendly vessels.

Compounding the supply challenge, shipbuilding delays and a slowdown in new orders since 2022 have hindered timely fleet renewal, increasing the risk of capacity tightness. Additionally, around 10% of the global fleet—mostly older ships—has been sidelined by sanctions and is likely to be scrapped, further tightening supply.

Geopolitical developments continue to disrupt trade. The Israel–Iran conflict and Saudi Arabia’s strategic shift toward domestic refining have reduced regional crude exports, impacting tanker demand. Meanwhile, U.S. crude exports have declined amid reduced global demand, tariffs, and pricing pressures.

Looking ahead, the IEA forecasts that global oil demand will peak in 2029, largely driven by Asia. This outlook continues to provide medium-term support for tanker demand, even as refining activity and trade flows shift geographically. Fleet renewal efforts are underway, with Hanwha Ocean and Greek operator Tsakos Energy Navigation planning to build up to three eco-friendly VLCCs for delivery by 2027.

NEWBUILDING – SALES & PURCHASE

April 2025 was characterized by continued caution in the tanker newbuilding and sale-and-purchase (S&P) markets. Persistent geopolitical tensions and regulatory uncertainty—particularly around sanctions and evolving environmental rules—kept investment sentiment subdued. Newbuilding activity remained limited, as shipowners delayed orders due to unclear decarbonization timelines and ongoing shipyard delays.

Activity in the Aframax and LR2 segments held relatively stable, supported by a preference for long-term charters to ensure revenue stability amid market volatility. Charter rates remained broadly in line with the previous quarter, but owners and charterers were selective regarding vessel type and specifications.

Despite the aging global fleet, the demolition market stayed quiet. Only a small number of older tankers were scrapped, as many shipowners continued to pursue life-extension strategies or upgrades rather than recycling. High freight rates and uncertainty about future regulations have discouraged scrapping, keeping older vessels in operation and further delaying fleet renewal.

Sanctions, particularly those targeting Iranian and Russian oil, continued to disrupt commercial flows and hinder investment. Iranian exports remained below expectations, while broader geopolitical tensions—such as those involving Russia—contributed to reduced tanker activity and strategic hesitation among market participants.

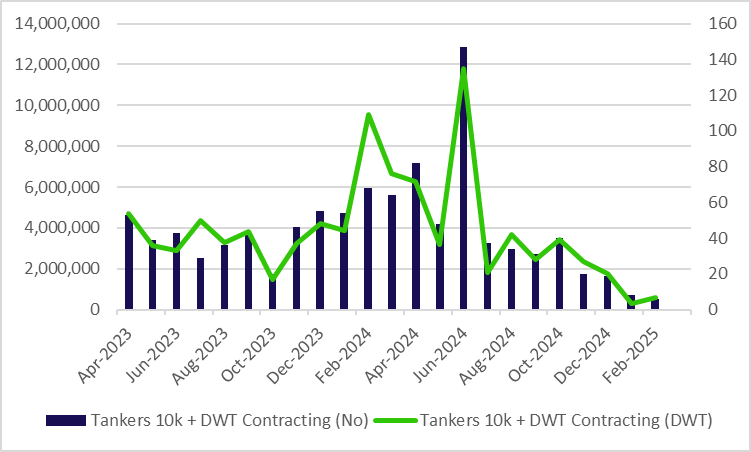

Graph 2: Tanker Newbuilding Contracts

The average age of the global tanker fleet is currently around 13–14 years, reinforcing the structural need for renewal. Despite this, shipowners remain cautious. Although interest in newbuildings is increasing, especially for eco-friendly designs, actual order placement remains limited due to economic and regulatory uncertainty.

Approximately 60–74% of new orders are being directed to Chinese shipyards, such as Yangzijiang and New Times Shipbuilding, which offer competitive pricing, shorter delivery times, and a reliable labor force—advantages over their South Korean and Japanese counterparts. Still, geopolitical frictions, including rising U.S. tariffs and supply chain uncertainties, have led many companies to postpone or scale back orders.

In the charter market, availability of larger tankers like VLCCs and Suezmax remains constrained. This supply tightness has helped sustain higher freight rates in those segments. Conversely, medium-sized vessels like Aframax and MR tankers have experienced softer demand and more mixed rate trends, creating an imbalance across size classes and further distorting market dynamics.

Graph 3: Total Tanker Sales

Ship recycling continues to be sluggish, with key demolition markets in India, Bangladesh, Pakistan, and Turkey showing limited activity. Contributing factors include seasonal and fiscal constraints, subdued scrap steel prices, and a general shortage of vessels available for scrapping due to the continued profitability of keeping older tonnage in service. Although the global steel market saw a minor price drop recently, anticipated demand and low inventories may soon reverse this trend, with implications for shipbuilding and maintenance costs.

Oil demand forecasts for 2025 remain mixed. BP and OPEC maintain a relatively optimistic outlook, while the IEA predicts slower growth, largely due to temporary economic headwinds in China. Market volatility is further fueled by international sanctions—particularly those affecting Iranian oil—which continue to rely on a shadow or “ghost” fleet, complicating global tanker availability and trade flow predictability.

In June 2025, tanker market activity remained cautious amid ongoing geopolitical uncertainty and regulatory challenges. Newbuilding orders stayed limited, with Greek shipowners leading investments in Handymax, MR, and Suezmax vessels featuring modern, eco-friendly designs.

Chinese shipyards such as Yangzijiang and New Times Shipbuilding continued to dominate newbuilding contracts due to competitive pricing and faster delivery, although rising tariffs and global tensions caused some owners to delay orders.

The demolition market remained subdued, as high freight rates and limited replacement options encouraged owners to keep aging vessels operational. Recycling activity in key markets like India, Bangladesh, and Turkey showed little improvement, affected by fiscal constraints and soft steel prices. Approximately 19% of the global tanker fleet is now over 20 years old, with many vessels being extended beyond typical service lifespans.

Geopolitical tensions, particularly the Iran–Israel conflict, kept freight rates and war risk premiums elevated. VLCC rates averaged around $60,000 per day, while insurance costs for 21-day stays in high-risk zones reached $40,000. Many owners continued rerouting vessels to avoid strategic chokepoints such as the Strait of Hormuz, resulting in longer voyages and increased operational costs.

DEMOLITIONS

Tanker recycling activity remained near historic lows through Q2 2025, reflecting a continuation of the subdued scrapping trend seen in recent years. Despite the aging global fleet and the upcoming enforcement of the Hong Kong International Convention (HKC) in June 2025, high freight rates and elevated vessel values have discouraged owners from retiring older ships.

Only a handful of tankers were recycled in the first half of 2025, extending the pattern seen in 2023 and 2024, where scrapping volumes hit record lows. Older tonnage continues to operate, often in sanctioned or high-risk trades, sustaining demand despite growing environmental and regulatory pressures.

Graph 4: Total Tanker Demolition

India has emerged as the primary destination for compliant recycling, with over 100 HKC-certified yards and efforts to align with stricter safety and environmental protocols. In contrast, Bangladesh and Pakistan remain underprepared, constrained by economic instability and limited certified capacity—particularly in Pakistan, where compliance gaps persist.

Following the Eid holidays, activity in South Asian yards remained quiet, with limited appetite from cash buyers and low availability of scrap tonnage. Meanwhile, recycling prices softened slightly due to weak steel markets, although broader structural demand remains.

The entry into force of the HKC marks a key turning point. While near-term activity is expected to remain muted, stricter rules may reshape global ship recycling practices and accelerate investment in compliant infrastructure—particularly in India. For now, however, owners remain cautious, balancing regulatory change with market incentives to keep aging vessels in service.

DRY BULK MARKET

FREIGHT MARKET

The second quarter of 2025 unfolded as a period of transition and strategic recalibration for global shipping markets, influenced by shifting seasonal demand, rising technological integration, and deepening geopolitical tensions. April traditionally marks the shift from winter energy demand to increased industrial and agricultural activity in the Northern Hemisphere, providing seasonal stability. However, in 2025, this balance was disrupted by escalating trade tensions between the United States and China. Washington’s decision to impose 145% tariffs on a wide range of Chinese imports was swiftly met with Beijing’s retaliatory measures amounting to 125%. These developments have already begun to distort global trade flows, particularly in the agricultural sector, and if further sanctions are implemented, dry bulk operators may need to realign routes to accommodate shifting export patterns.

On the technological front, the shipping industry made significant strides in digitalization and automation. In May, Eastern Pacific Shipping (EPS), in partnership with Avikus, deployed autonomous navigation systems on two vessels—a suezmax and a bulk carrier. The systems integrate AI-powered route planning, fuel optimization, and shore-based monitoring via the HiNAS Cloud platform. This marks the first commercial retrofit of such technology outside of Korea and reflects a growing industry trend toward smarter, safer, and more efficient operations.

Graph 5: Baltic Indices

Building on this momentum, Pacific Basin announced in June the installation of Inmarsat’s NexusWave high-speed internet on five of its geared Handysize and Supramax bulk carriers. With download speeds exceeding 330 Mbps and 99.9% uptime reliability, the system improves real-time operational efficiency and supports crew welfare. This deployment is part of Pacific Basin’s broader digital transformation strategy, and its timing coincides with the broader market demand for connectivity, as more than 1,000 vessels globally have now ordered NexusWave systems.

Meanwhile, structural shifts in global demand continue to shape the dry bulk market. The accelerating adoption of electric vehicles is increasing the need for raw materials like copper and nickel, boosting demand for bulk carriers, particularly in the Supramax and Panamax segments. This trend has supported freight rates and increased vessel utilization, although gains remain uneven across vessel classes. Notably, the Capesize segment continues to struggle due to weak Chinese steel demand and broader macroeconomic uncertainty, despite the segment’s tight supply.

Overall, Q2 2025 highlighted the growing complexity of the maritime landscape. While technological advancements and green demand drivers offer new opportunities, volatility in trade policy and persistent economic caution are creating mixed signals. The months ahead are likely to be shaped by how quickly trade realigns, how broadly autonomous and digital solutions scale, and whether demand in the Capesize segment recovers alongside any improvement in global industrial output.

NEWBUILDING – SALES & PURCHASE

The dry bulk sector in Q2 2025 continued to face a cautious investment environment, with newbuilding activity slowing notably. Bulk carrier orders declined by 26% year-on-year during the first half of 2025, as persistently low freight rates, combined with elevated construction costs, deterred new commitments. Shipowners remain

hesitant to place new orders, especially as uncertainty looms over potential U.S. port fees targeting Chinese-built vessels.

Geopolitical trade policy also influenced vessel transactions. Anticipation of tariffs on Chinese-built ships—pending a final decision by the U.S. administration—has sharply reduced buying and selling activity involving Chinese tonnage. In contrast, secondhand transactions involving Japanese and South Korean-built bulk carriers have increased during the same period. Greek shipowners remained particularly active in the secondhand bulk carrier market, accounting for over 55% of all purchases in this segment, as they continue to expand and modernize their dry bulk fleets opportunistically.

Graph 6: Bulkcarrier Newbuilding Contracts

Fleet renewal efforts are evident in recent transactions. In May, Jinhui Shipping sold the 2008-built Supramax Jin Tong for approximately $10.2 million, marking its second sale of the year. The sale is part of the company’s ongoing strategy to optimize fleet age and efficiency, leaving Jinhui with a fleet of 32 bulk carriers—25 of which are owned.

Although containership orders surged in Q2, bulk carrier contracting lagged, with few new orders placed globally. The Greek newbuilding focus in June was largely directed toward tankers and containerships, pushing Greece to the third position globally in total ship orders. However, bulk carrier orders continued to decline, reflecting broader hesitancy in the sector despite solid secondhand demand.

Graph 7: Total Bulkcarrier Sales

The ship sales market remained stable throughout Q2. While newbuilding slowed, secondhand bulk carrier transactions proceeded steadily, reflecting continued investor confidence in asset values and long-term demand fundamentals. Despite global macroeconomic uncertainty, the dry bulk market showed signs of selective, disciplined investment activity—especially in the resale and fleet renewal segments.

DEMOLITIONS

The dry bulk scrapping market maintained a steady, albeit slower, pace in Q2 2025 compared to the previous year. Despite the aging profile of the global fleet, scrapping activity has not accelerated as expected. This is largely due to relatively firm secondhand prices, moderate freight rates, and owners’ reluctance to dispose of older vessels in a market still marked by macroeconomic uncertainty and geopolitical disruptions.

Demolition volumes for bulk carriers have declined compared to 2024, even though the fleet’s average age continues to rise. As of June 2025, the average age of the global bulk carrier fleet stands at 12.4 years—up by nearly two years from January 2021. This upward shift reflects deferred retirement of older tonnage and limited newbuilding replacements, especially in the smaller and mid-sized bulk carrier segments.

In May, Star Bulk Carriers, a Nasdaq-listed company based in Athens, announced the sale of five older Supramax vessels as part of its ongoing fleet renewal strategy. These disposals were aimed at improving overall fleet efficiency and emissions performance in light of tightening environmental regulations. Following the sale, Star Bulk retains a fleet of 132 vessels, with 115 fully owned, maintaining its position as one of the leading players in the global dry bulk sector.

The market’s cautious approach to demolition also reflects challenges in key recycling hubs. South Asian scrapping yards, especially in Bangladesh and Pakistan, continue to face financing constraints, weak steel prices, and limited access to HKC-compliant facilities. Although India remains the leader in compliant recycling capacity, activity has remained subdued due to a lack of eligible candidates and owners’ preference to trade aging tonnage longer.

Graph 8: Total Bulkcarrier Demolition

Looking ahead, stricter decarbonization and lifecycle emissions standards—combined with the enforcement of the Hong Kong Convention—are expected to gradually reshape the dry bulk fleet profile. However, unless freight markets weaken significantly or regulatory enforcement tightens further, scrapping activity in the second half of 2025 is likely to remain modest, with owners opting for life-extension strategies over immediate demolition.

CONTAINER MARKET

FREIGHT MARKET

The second quarter of 2025 was marked by continued volatility in the containership freight market, with short-lived rallies, persistent uncertainty, and sharp route-specific fluctuations. While the quarter offered glimpses of recovery—particularly in May and early June—the broader picture remains one of fragility and imbalance, shaped by macroeconomic pressures and evolving geopolitical dynamics.

In April, the market showed tentative signs of stabilization, following a period of weak demand and declining rates that defined much of the previous year. A modest upswing in rates was observed on key trade lanes—especially between Asia and the United States—driven by renewed geopolitical tensions, including escalating tariff threats between Washington and Beijing. However, this brief recovery proved unsustainable. By the final week of April, rates had softened once again, reaffirming the market’s vulnerability and its dependence on external factors such as trade policy shifts, inventory cycles, and consumer demand in major economies.

Graph 9: Containers Freights and Earnings

May continued this pattern of fluctuation, with freight rates rising and falling in response to shifting sentiment and demand levels. The most notable improvements occurred on transpacific routes, particularly in the second half of the month, where rising U.S. import volumes led to stronger vessel utilization and improved spot rates. This upward trend fostered cautious optimism across the sector, suggesting that a bottom may have been reached in some segments of the market. However, the recovery remained uneven, with other trade lanes—such as intra-Asia and Asia–Europe—showing less pronounced gains.

June opened on a strong note, buoyed by the momentum from late May. Spot rates on China–US and China–Europe routes surged amid increased bookings and port congestion in parts of East Asia. Yet this rally was short-lived. As June progressed, signs of weakening demand began to emerge, particularly in the U.S. market, where macroeconomic uncertainty—including concerns over consumer spending, interest rates, and retail inventories—contributed to reduced booking volumes. This reversal placed renewed pressure on major east–west trades, eroding earlier gains.

Despite the mid-month softening, spot rates in late June remained significantly higher than those observed in early spring, leaving some room for cautious optimism heading into Q3. Market sentiment, however, remains fragile, with charterers and carriers alike maintaining short-term strategies in response to uncertain demand visibility and ongoing geopolitical friction.

NEWBUILDING – SALES & PURCHASE

Despite geopolitical headwinds—particularly escalating U.S.–China tariff disputes—the containership newbuilding market continued to expand significantly during Q2 2025, driven by long-term planning, fleet modernization goals, and environmental compliance pressures. Orders remained strong throughout the quarter, with major carriers and shipowners committing to large, next-generation vessel programs.

In April, South Korea’s HD Korea Shipbuilding & Offshore Engineering (HD KSOE) secured contracts for 24 new containerships from various Asian and Oceanian operators. The first tranche included 20 vessels of varying sizes: four with a capacity of 8,400 TEU, eight with 2,800 TEU, and six with 1,800 TEU. These ships are scheduled for delivery in the first half of 2028. Additionally, HD KSOE signed a separate deal for two more boxships valued at approximately $400 million. Samsung Heavy Industries also secured an order from an Asian shipowner for two containerships worth $358 million, to be delivered by January 2028. These contracts underline Korean yards’ continued leadership in high-value, technologically advanced containership construction.

Graph 10: Containerships Newbuilding Contracts

In May, the orderbook expanded further as OOCL placed a landmark order for 14 large containerships valued at over $3 billion with COSCO-affiliated Chinese shipyards. Deliveries are expected between 2028 and 2029. Although fuel specifications were not disclosed, the investment reflects OOCL’s long-term commitment to scale and efficiency. In parallel, Hapag-Lloyd announced an order for six dual-fuel (conventional and LNG) containerships of 16,000 TEU each, placed with Hengli Heavy Industry and Fujian Mawei shipyards in China. These vessels are set for delivery around 2027.

Momentum continued into June, as Ocean Network Express (ONE) ordered eight 16,000 TEU dual-fuel vessels from Hyundai Heavy Industries in South Korea, reaffirming its strategy to modernize and decarbonize its fleet. At the same time, Seaspan, a major lessor and member of the Atlas Group, ordered six 8,300 TEU methanol-fueled containerships from Hudong-Zhonghua shipyards in China. These vessels are expected to be chartered to COSCO, indicating strong liner support for alternative fuel propulsion. Also in June, HD Hyundai Samho Heavy Industries (a subsidiary of HD KSOE) announced an order for two dual-fuel boxships worth $280 million, with delivery scheduled for March 2028.

Completing a major investment cycle, Hapag-Lloyd took delivery of the final vessel from its 12-ship dual-fuel program, marking the conclusion of one of the most significant recent containership renewal efforts in the sector.

Graph 11: Total Containership Sales

The Q2 2025 containership order boom reflects a long-term focus on capacity expansion, emissions compliance, and operational flexibility. The strong demand for dual-fuel and methanol-powered vessels highlights a clear shift toward greener propulsion, while delivery timelines extending into 2028–2029 suggest that the sector anticipates continued growth in global container volumes and stricter regulatory requirements. Despite short-term freight rate volatility, carrier strategies appear firmly anchored in long-term resilience and environmental transition.

DEMOLITIONS

Containership demolition activity remained exceptionally subdued in Q2 2025, continuing the broader trend of limited scrapping across vessel segments. In April, scrapping volumes reached one of the lowest levels on record, with just three vessels sold for demolition—each to different countries: India, Turkey, and Singapore. This near standstill reflects both strong asset values and the broader market disruption caused by escalating trade tensions.

Graph 12: Recycling Market Price

A key contributing factor to the slowdown was the sudden imposition of steep U.S. tariffs on Chinese-built ships and a wider range of goods. The abrupt policy shift generated uncertainty across global supply chains and prompted owners to delay disposal decisions, opting instead to retain aging vessels amid shifting trade flows and temporarily firming charter markets.

While scrapping levels typically increase when freight rates soften, current demolition trends remain disconnected from short-term rate signals. High residual values, cautious sentiment, and long delivery schedules for newbuilds are all supporting vessel retention, even for older tonnage.

As the Hong Kong International Convention (HKC) comes into force later in 2025, the demolition landscape is expected to change—particularly in terms of environmental compliance and yard selection. However, in Q2, the containership scrapping market remained stagnant, reflecting both market uncertainty and the sector’s ongoing preference to trade, rather than recycle, aging capacity.

LNG/LPG MARKET

FREIGHT MARKET

The second quarter of 2025 brought significant fluctuations to the LNG shipping market, reflecting a complex mix of oversupply, underwhelming seasonal demand, and delayed project activity. In April, spot charter rates for modern 174,000 cbm LNG carriers plunged to historic lows. Rates in the Atlantic Basin dropped as low as $3,500/day, while the Pacific market saw modestly higher levels around $11,000/day. Freight rates for LNG cargoes originating from the U.S. Gulf Coast ranged from $0.67/MMBtu to Northwest Europe to $1.52/MMBtu to Asia, highlighting continued regional imbalances.

These exceptionally low rates were largely driven by a glut of available tonnage—with 96 new LNG carriers expected to be delivered throughout 2025—alongside delays in several high-profile liquefaction projects. Additionally, the tail end of winter left inventories high and demand relatively soft across key Asian and European markets, undermining spot activity.

In May, the LNG market showed tentative signs of stabilization. Spot charter rates in the Atlantic edged up slightly to around $4,000/day, a marginal improvement but still well below sustainable levels. This modest rebound was attributed to slight tightening in vessel availability and early signs of restocking demand from Asian buyers. Despite this uptick, the market remained fragile, with limited visibility on short-term gains.

Graph 13: LNG Spot Rates

The LPG sector, in contrast, remained relatively steady throughout the quarter. Rates for Very Large Gas Carriers (VLGCs) trading on the Middle East to Far East route held firm, averaging between $85–$90 per metric ton in both April and May. The stability reflects continued strong demand for propane and butane in Asia, coupled with healthy U.S. export volumes and limited fleet growth.

By June, LNG spot charter rates continued their gradual recovery. Atlantic Basin rates for 174,000 cbm vessels rose to approximately $4,250/day, maintaining the upward trajectory observed since April. While still subdued relative to historical norms, the trend points to a slow rebalancing of supply and demand, with sentiment improving ahead of the winter contracting season. Market participants are increasingly optimistic about a rebound in global LNG trade flows in the second half of 2025, especially as delayed U.S. liquefaction projects begin to ramp up output.

Despite ongoing near-term volatility, the long-term fundamentals for both LNG and LPG shipping remain positive. As natural gas plays a transitional role in the global energy mix, investment in liquefaction capacity and infrastructure continues to expand, supporting vessel demand over the medium to long term. In the LPG segment, structural demand from Asia and increased petrochemical activity are expected to keep freight levels resilient. While oversupply in LNG tonnage may continue to weigh on spot rates in the coming months, charter activity and forward bookings suggest that the worst may have passed, and a gradual recovery is underway.

NEWBUILDING – SALES & PURCHASE

The second quarter of 2025 confirmed the continuing strength of the newbuilding market for LNG and LPG carriers, underpinned by decarbonization strategies, regulatory pressure, and sustained long-term demand for cleaner fuels. While sale and purchase (S&P) activity remained muted throughout the quarter, shipowners clearly favored fleet renewal through technologically advanced newbuilds over secondhand acquisitions.

Graph 14: LNG/LPG Sales

In April, newbuilding momentum remained firm. Key deliveries included the Aquamarine Progress II and Russia’s Alexey Kosygin, reinforcing the trend toward dual-fuel and emissions-compliant designs. The LNG sector maintained its leadership in orders, with a record 78 newbuilds placed in 2024, nearly doubling the previous year’s total. This signals a clear industry shift toward next-generation propulsion, including dual-fuel LNG and LPG systems, methanol-ready engines, and enhanced energy efficiency features.

The pace held steady in May, with further deliveries such as the Pacific Astra—a 174,000 cbm dual-fuel LNG carrier—and two medium gas carriers (MGCs) from South Korean shipyards. Orderbooks reflected robust demand for dual-fuel LNG and LPG vessels with delivery slots extending into 2027–2028, as shipyards operated near capacity. Environmental compliance and tightening IMO regulations, including CII and EEXI enforcement, continued to drive order placement strategies.

June sustained this momentum, with additional orders for LNG and LPG carriers recorded across Korean and Chinese yards. Multiple dual-fuel vessels were delivered, reinforcing the industry’s transition to greener fleets. Owners prioritized long-term decarbonization goals, with fleet renewal planning shaped by both environmental requirements and anticipated supply-demand imbalances in global gas markets.

In contrast to the active newbuilding sector, the S&P market remained quiet throughout Q2. In the LNG segment, secondhand activity was minimal as owners focused on securing long-term charter contracts and avoided divesting modern tonnage, particularly amid a volatile spot market and high newbuild valuations.

Graph 15: LNG & LPG Newbuilding Contracts

The LPG S&P market saw slightly more movement, particularly involving modern Very Large Gas Carriers (VLGCs) and Medium Gas Carriers (MGCs) equipped with dual-fuel or eco-efficient engines. These isolated deals were often driven by strategic repositioning or asset rotation, rather than speculative investment.

By June, transactional volume had not materially increased, though sentiment improved slightly. The S&P market is expected to pick up moderately in the second half of 2025, particularly for LPG carriers, as asset prices stabilize and older vessels are phased out or repurposed in anticipation of the next freight cycle.

DEMOLITIONS

The demolition and recycling market for LNG and LPG carriers remained virtually inactive throughout the second quarter of 2025, continuing a trend of extremely low scrapping activity across the gas shipping sector.

In April, no notable demolition transactions were recorded. High market demand for gas carriers, coupled with a shortage of viable scrap candidates, discouraged vessel retirement. Even older tonnage remained commercially attractive, with many units undergoing retrofits or life-extension maintenance to comply with tightening environmental standards such as the IMO’s Carbon Intensity Indicator (CII) and Energy Efficiency Existing Ship Index (EEXI). As such, scrapping decisions were deferred by most owners in favor of preserving capacity amid a still-developing freight recovery.

Graph 16: Total LNG Demolition

This pattern continued in May, with recycling activity near zero for both LNG and LPG fleets. Owners prioritized operational flexibility over asset disposal, especially as many vessels remain structurally sound and capable of compliance through technical upgrades. The limited appeal of demolition was reinforced by the robust forward outlook for gas transport and a lack of urgent regulatory enforcement requiring phase-outs. Without major market or policy shifts, scrapping remained economically unattractive.

In June, the situation remained largely unchanged. Despite the aging profile of parts of the fleet—especially for LPG carriers—there was no significant increase in scrapping, as charter rates remained supportive and newbuild delivery bottlenecks encouraged the retention of older units. Unless there is a material drop in market returns or a regulatory event forcing asset retirement, demolition activity in the LNG and LPG segments is expected to remain muted through the summer and possibly beyond.

SUSTAINABILITY

NEWS

The second quarter of 2025 highlighted the growing tension between accelerating global shipping activity and the urgent need to decarbonize. As emissions targets remain unmet and climate deadlines loom, maritime stakeholders pushed forward with a range of technological, regulatory, and collaborative initiatives aimed at greening the industry.

In April, concerns mounted over the failure of EU member states to meet even minimal climate targets, such as the IMO’s 20% emissions reduction by 2030. The lack of a robust carbon levy and insufficient financial support has placed disproportionate pressure on developing nations. In contrast, countries in the Global South have taken bolder stances, demanding equitable solutions and pledging independent climate actions.

The complexity of transition remains high, with evolving regulations like the EU ETS, FuelEU Maritime, and IMO’s targets reshaping route planning and fuel strategies. Technological innovation continues to provide a pathway forward. Wärtsilä, in collaboration with Chevron Shipping, introduced a methane slip reduction solution for its 50DF engines, cutting methane emissions by 75% while improving efficiency. CMB.TECH and Fortescue agreed to charter a dual-fuel ammonia-powered bulk carrier for delivery by 2026, while Maersk added the methanol-fueled “Arthur Maersk” to its fleet. Similarly, MOL took delivery of the methanol-fueled “Verde Heraldo”, reflecting increased confidence in alternative fuels despite fuel availability concerns.

Meanwhile, BIMCO and ASBA launched a modernized 2025 edition of the ASBATANKVOY charter party to meet new legal and regulatory standards. Greek shipowners led investment in alternative propulsion, with the world’s largest LNG-fueled fleet share (7.3%) and a 66% scrubber installation rate on tankers under construction.

May brought further momentum to maritime decarbonization. Wärtsilä unveiled its NextDF engine platform, reducing methane slip to under 1.4% and improving NOx emissions. It also completed the world’s first full-scale onboard carbon capture installation, offering up to 70% CO₂ reduction and compatibility with existing vessels. ABS issued new guidelines for safe ammonia and hydrogen use, and highlighted dual-fuel propulsion safety standards. Simultaneously, TotalEnergies and Lloyd’s Register integrated AI in the OneOcean platform, optimizing voyage planning and reducing CO₂ emissions by over 2,200 tons.

New tech also emerged in auxiliary systems: Corvus Energy delivered advanced battery systems for Matson’s hybrid LNG-powered containerships, and refrigerated container innovations promised a 3.7-million-ton CO₂ reduction annually. The UAE launched the “Blue Pass” digital platform for transparent bunkering, while initiatives like onboard particle sensors and biofouling management plans gained traction.

Regulatory frameworks evolved, too. From May, the Mediterranean Sea became part of an Emission Control Area (ECA), cutting sulfur limits to 0.1%. The IMO prepared mid-term measures (for 2028 onward), including carbon pricing and green fuel incentives. Parallel to this, the EU ETS expanded its scope and GCMD, in cooperation with the ADB, invested in green maritime finance.

Notably, electrification and AI-driven shipbuilding made headlines. Scandlines tested its first electric ferry in Turkey. HD Hyundai launched a robotic welding shipyard initiative in partnership with Persona AI and Vazil. Japan’s University of Tokyo spearheaded a five-year research initiative to develop materials for energy infrastructure, supported by companies like Kobe Steel and Nippon Steel.

Collaborations surged. Anemoi Marine, Hafnia, GSI, and DNV launched a joint project to equip MR tankers with Rotor Sails. NYK introduced Japan’s first marine biodiesel antioxidant, while MAN Energy unveiled the world’s most powerful methanol-fueled engine. At the infrastructure level, the Port of Aalborg and NORNE announced a new CO₂ hub with EU backing.

In June, innovation expanded across all fronts. Latin America launched its first fully electric tug in Chile, while retrofit upgrades gained popularity. Lloyd’s Register, CoolCo, and HD Hyundai Mipo retrofitted the Kool Glacier LNG carrier with sub-coolers, enhancing boil-off reliquefaction. Hoegh Autoliners joined the Sustainable Markets Initiative, and Auramarine released sensors for measuring water content in methanol fuel.

The Alternative fuels broadened, with ethanol and ammonia gaining traction. GTT received DNV approval for membrane tanks rated at 1 barg for LNG-fueled ships, and MOL received Approval in Principle (AiP) for LNG carriers fitted with solid oxide fuel cells. Simultaneously, Alfa Laval launched Aalborg marine boilers with hybrid capabilities, and Ecospray’s carbon capture system reached commercial readiness.

Wind propulsion matured. Union Maritime delivered the first tanker fitted with BAR Technologies’ WindWings, while Lloyd’s Register validated their effectiveness with the TR Lady. The new “WindWings Hub” by BAR will aggregate data to improve adoption and performance benchmarking. In parallel, Corvus Energy and HD Hyundai Mipo gained AiP for a green product tanker, while KNCC’s innovative LCO₂ carrier concept also received classification approval.

Infrastructure development continued. K LINE and Yinson Production advanced floating CO₂ storage units, while Elomatic and Mitsubishi Shipbuilding agreed to jointly develop digital decarbonization solutions. Avikus and ZeroNorth partnered to integrate autonomous navigation and voyage optimization. Japan’s TRE Holdings also began feasibility studies on commercial green methanol production from biomass.

Digital transformation and connectivity saw upgrades as Inmarsat’s NexusWave platform rolled out to Pacific Basin bulkers, delivering data speeds up to 340 Mbps. Additionally, WinGD secured orders for ammonia-powered engines for vessels chartered by Trafigura, and Whitaker Tankers introduced the first FAME B100-certified blending bunker vessel. In another milestone, Hyundai unveiled a 40,000 CBM LCO₂ carrier in collaboration with Capital Gas and DNV.

The quarter ended with regulatory and environmental progress. The Port of Piraeus welcomed COSCO’s “Yuan Hai Kou”, a 7,000-vehicle green PCTC vessel. Meanwhile, the Hong Kong Convention for safe ship recycling entered into force, and fifteen European environment ministers agreed to phase out scrubber discharge in the Northeast Atlantic by 2029, solidifying the region’s status as a global Emission Control Area.

Collectively, Q2 2025 reflects the maritime industry’s growing commitment to low-carbon fuels, smart technologies, and cross-sector collaboration. Yet, the road to decarbonization remains uneven. Infrastructure gaps, regulatory delays, and market fragmentation persist. However, innovation and cooperation across the industry signal cautious optimism for meeting climate goals, if momentum is sustained and globally aligned.