Alan McCarthy (left) and Andrew Hampson.

Developments in capital markets for shipping – IMIF learns secrets behind Tufton’s novel $91m deal

An “alignment of the planets” enabled success in what was the first pure shipping play in the specialist funds segment of the London Stock Exchange.

These nine “planets” are part of the in-house criteria for evaluating potential investments carried out at Tufton Oceanic, a fund management company specialising in the maritime, offshore and energy industries with just under $1.5bn assets under management of which $1bn is invested or available for investment in vessels.

The presentation begins.

Andrew Hampson, managing director at the firm for asset-backed investments, said that he favoured a selection of metrics other than calculations based on present and predicted freight rates, which many others in the shipping finance field used.

He was speaking at a meeting in London on April 13, 2018, of the International Maritime Industries Forum.

Mr Hampson said that Tufton’s approach was designed to appeal to certain clients: “we are not dealing with traditional shipping investors; we are talking to people who are interested in other things. These people say, very basically, ‘what is the industry worth?’”

Tufton’s innovative $91m fund-raising, half of which has already been invested in container tonnage, was tailored for the specialist funds segment of the exchange which according to its official description is “designed for highly specialised investment entities that wish to target institutional, highly knowledgeable investors or professionally advised investors only.”

The planets align.

One reason that Tufton went to that part of the market was that shipping was new to it, “and I think shipping investors got fed up with the way they were treated in some of the capital markets. This is a very clear, easy market and transparent on costs.” It compared with high fees in the New York market. Mr Hampson clarified: “We don’t go to traditional equity spaces.”

Tufton’s sourcing of capital has been from private entities, almost entirely non-shipping investors who have been involved with rail, aircraft, housing, retail and other sectors. This meant that the business model here was “you have to look at returns the whole time.”

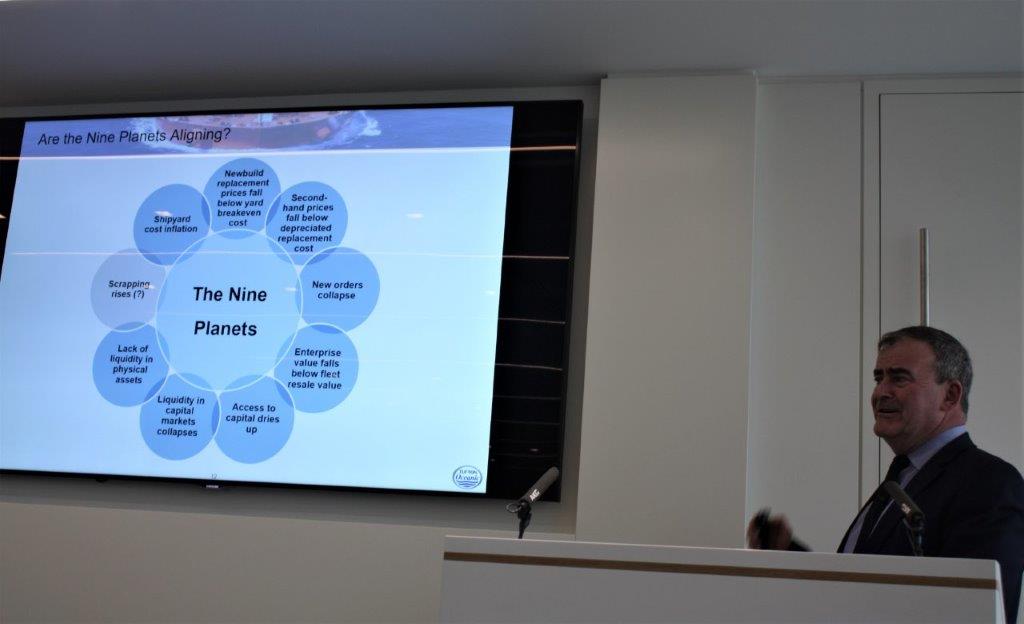

It involved meeting specific conditions for investment, which Tufton dubbed the “nine planets.”

These features could be summed up as newbuilding prices below or at breakeven cost; second-hand prices below depreciation or replacement cost; new orders collapsing as a percentage of the fleet; enterprise value below fleet resale value; access to capital drying up; liquidity in the capital markets; liquidity in physical assets in the second-hand market; vessel scrapping; and shipyard cost inflation in terms of price of steel and equipment and the dollar value of Asian labour.

Earlier, he referred to the general climate for ship finance. Shipping had become less attractive to the capital markets consistently for the last seven to eight years, with an ongoing decline in the amount of market funding.

An overall fall in leverage over the period had been part of the dramatic decline, mainly seen in an exit from issuing bonds. The contribution of funding to shipping had fallen, according to Marine Money, from $54bn in 2011 to $19bn in 2017.

Main funding for the international fleet was coming from bank debt, 35% of the total, with only 4% funded by private equity, according to analysis by Clarkson Research Services and Tufton. In 2010 the bank figure had been 50% and private money had played a much greater role than now.

“Over 10 years, we have lost $150bn of bank debt funding in the industry, much of that reflected by the fall in value of the fleet itself.”

Although the leading Chinese leasing companies had put in some $50bn, led by ICBC Leasing, some Chinese lessors were starting to have issues in their portfolios, and of this source Mr Hampson said: “I think it will become potentially less competitive.”

He referred to Clarkson figures showing that the world fleet on the water as at March 2018 was worth an estimated $784bn. Adding all reported orders, the figure rises to $1 trn. Ten years ago, the value of vessels on the water was $725bn, and when the newbuilding orderbook at that time is added, the total for comparison to the $1trn today was $1.1trn.

The fleet on the water had grown some 21% to 600m dwt since the peak of its valuation in 2013. At the same time, its value has decreased by about 14%.

Tufton funds own outright 73 vessels, nearly all without bank debt, across all shipping sectors, and the group has substantial private holdings, in Hafnia Tankers and Gram Car Carriers.

In an initial public offering on the London exchange in December 2017 it raised $91m for a Guernsey-based investment trust named Tufton Oceanic Assets Ltd (SHIP.L).

SHIP.L aims to invest into a diversified portfolio of second-hand cargo-carrying vessels with an emphasis on medium to longer term charters. It can take on leverage at special purpose vehicle level but does not depend on doing so, said Mr Hampson. So far, some 51% of the amount raised has been invested in four containerships, and Mr Hampson said that the business was reviewing investment in other sectors.

The target distributed yield of the new vehicle is 7%, and the long-term target internal rate of return is in the region of 12%.

Alan McCarthy, the IMIF chairman, commented: “I would guess this is a unique approach to shipping investment” and many in the audience said they were impressed that Tufton had been able to carry out a fund raising of this nature in the London market.

Asked about shipmanagement arrangements, Mr Hampson said that Tufton has a manager in Cyprus that handles commercial and technical activities, most of which are outsourced.

Mr Hampson, who has played a leading role in reinforcing Tufton’s position as a dedicated fund manager in shipping assets. said that Tufton was “on plan to meet prospectus targets.”

The IMIF meeting was hosted by law firm Ince & Co.