CEO Stefan Ermisch

Solid 2018 financial year for Hamburg Commercial Bank

– Group net result before taxes of € 97 (-453) million

– CET1 ratio improved further to 18.5 (15.4)%

– Administrative expenses lowered by 16%

– CEO Ermisch: “Driving transformation forward; becoming profitable”

Hamburg – Hamburg Commercial Bank AG closed out the 2018 financial year with a positive result, solid new business and strong capital ratios. The Bank furthermore successfully completed its privatization, reduced its costs significantly and almost entirely shed its legacy assets. Hamburg Commercial Bank is thereby at the beginning of a profound multi-year transformation, for which key parameters were already set in 2018.

“We generated a respectable Group net result in the ground-breaking year of 2018, despite all the uncertainties and difficulties in the wake of privatization. We will now do everything to develop our Bank into an appropriately profitable one. To do so, we shall continue to resolutely drive forward the transformation that has already begun with all our energy. Our objective is to be a more efficient and responsive Bank, which places the client centre-stage more than ever and generates added value for its shareholders,” said Stefan Ermisch, CEO of Hamburg

Commercial Bank.

Exceptional factors and privatization affect Group net result

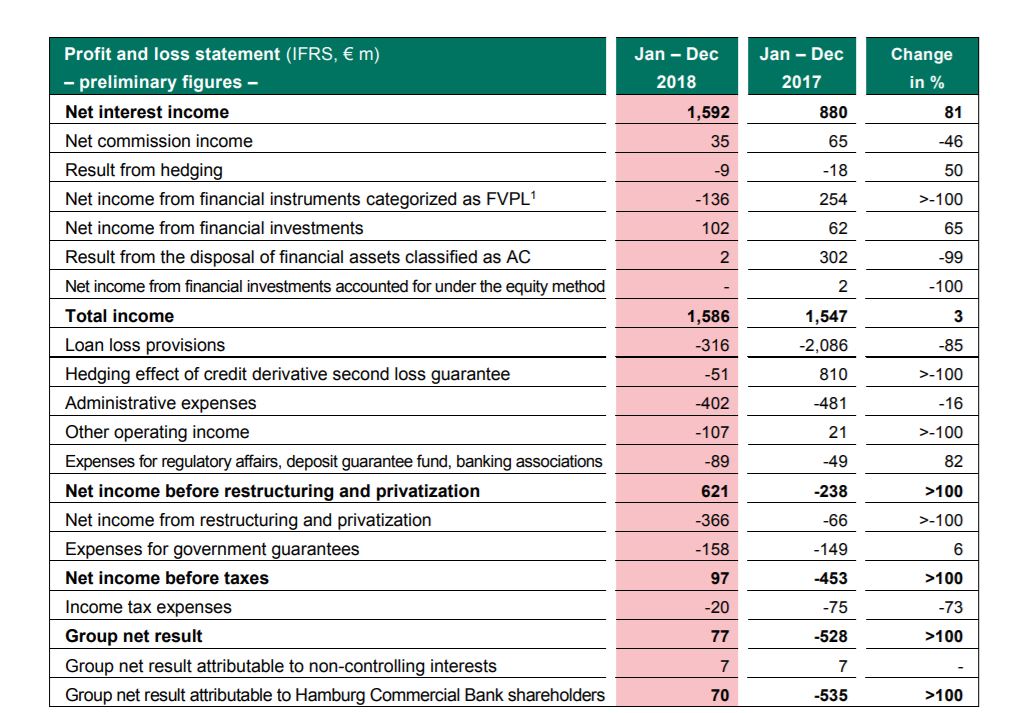

The net income before taxes of € 97 (-453) million benefited from good performance in the operating business just as it did from successful cost savings. Exceptional factors involving the realigned asset and liabilities side of the balance sheet and heavy privatization costs also affected the Group net result. The expenses for restructuring the Bank alone had a negative impact of € -366 (-66) million on the result. The guarantee fees which were applied for the final time in 2018 and the once-off payment for terminating the guarantee had an impact of € -158 (-149) million. After taxes, the Group net result came to € 77 (-528) million.

The Group’s total income rose slightly to € 1,586 (1,547) million and was underpinned by net interest income amounting to € 1,592 (880) million, which, alongside income from the operating business, also includes revaluations of hybrid financial Instruments.

New business virtually at previous year’s level

With a sum of € 8.4 (8.6) billion, new business virtually matched the previous year’s level and the margins already clearly reflected the Bank’s sharp focus on profitability. In the Real Estate Clients segment, newly signed business amounted to € 4.6 (4.7) billion; in Shipping it was € 1.0 (0.5) billion. Finance for corporate clients was scaled back considering the competitiondriven pressure on margins and the segment concluded new business amounting to € 2.8 (3.1) billion.

On the cost side, the Bank achieved further success and lowered administrative expenses by 16% to € -402 (-481) million. Personnel expenses dropped to € -198 (-230) million and reflect the reduced number of 1,716 Group employees (31/12/2018: 1,926 full-time employees).

Operating expenses were down to € -186 (-215) million and depreciation of tangible assets fell to € -18 (-36) million.

Conservative loan loss provisioning – CET1 ratio improved again

With a view to the mounting economic uncertainties in Europe and possible worldwide trade disputes as well as for individual exposures, the Bank set aside loan loss provisions amounting to € -287 (-1,402) million and thereby maintained its conservative approach. In the previous year, significant additions for legacy loans weighed heavily on loan loss provisioning.

After currency effects as well as final compensation for and the hedging effect of the credit derivative involving the now terminated guarantee, loan loss provisioning totalled € -367 (-1,276) million.

The non-performing exposure ratio dropped to about 2% (end of 2017: 10.4%) because of the virtually complete disposal of non-performing loans in the wake of privatization. The coverage ratio for non-performing loans stood with 57.6% at the end of the year at a good level.

The CET1 ratio improved further year-on-year to 18.5% (end of 2017: 15.4%) and is therefore at a very high level, also compared with the market. A particular contributing factor was the reduction in risk-weighted assets (RWAs), which was due to the declining business volume in the Non-Core Bank and lower market risks. The leverage ratio solidified at a good level of 7.4 (7.7) % that far exceeds the regulatory requirements.

Total Group assets were down as expected by about one fifth to € 55 (70) billion due especially to the disposal of non-performing legacy loans.

Outlook

The Bank anticipates a modestly positive IFRS-based Group net result before taxes for the 2019 financial year, subject to unforeseeable effects arising from the restructuring.

“We will be focusing this year on raising our operating performance and intend to significantly increase our profitability. To that end, we shall rapidly and stringently continue the profound transformation of our Bank,” said CEO Stefan Ermisch.