Peter Sand

BIMCO December Market Outlook: Tanker shipping and Macroeconomics 25 Nov. 2019

MACROECONOMICS

World growth and trade volumes under pressure, but still positive

A continued slowdown in global growth, as well as a lower trade multiplier will reduce overall demand for shipping for the rest of this year and through 2020.

Expectations for global trade growth have also been lowered for 2020; this is now forecast at 2.7%, down from 3%. The WTO cautions that risks to these forecasts are weighted to the downside, with these risks including a potential deepening of trade tensions, financial volatility and rising geopolitical tensions in many regions of the world.

World goods trade grew by only 0.6% in the first half of 2019, with the WTO expecting a slight recovery in the second half of the year in order for volumes to reach the projected growth of 1.2%, which reflects normal seasonality from a shipping perspective.

World goods trade grew by only 0.6% in the first half of 2019, with the WTO expecting a slight recovery in the second half of the year in order for volumes to reach the projected growth of 1.2%, which reflects normal seasonality from a shipping perspective.

BIMCO reiterates that raising tariffs is bad not only for the economies directly involved, and shipping between them, but also for the global economy and trade as a whole.

TANKER SHIPPING

Sky-high freight rates have given way to a profitable winter market supported by the fast-approaching IMO 2020 Sulphur Cap

BIMCO expects freight rates will once again come under pressure after the end of the high seasonal demand in Q4, as well as the boost from the sulphur cap. The fleet growth of 6.3% in the crude oil tanker market and the 4.8% growth in the oil product fleet will have its consequences on the supply and demand balance.

Demand drivers and freight rates

Reported very large crude carrier (VLCC) earnings reached USD 307,888 per day on 11 October, although the following week they fell as quickly as they had risen. After the drop, rates stood at USD 74,681 per day on 1 November which, aside from the recent peak, is the highest level since early 2016.

So what drove up the rates in October? Geopolitics is the simple answer. The slightly more detailed response is that geopolitics and the refiners’ need for crude ahead of the 2020 sulphur cap on 1 January created a hefty demand cocktail.

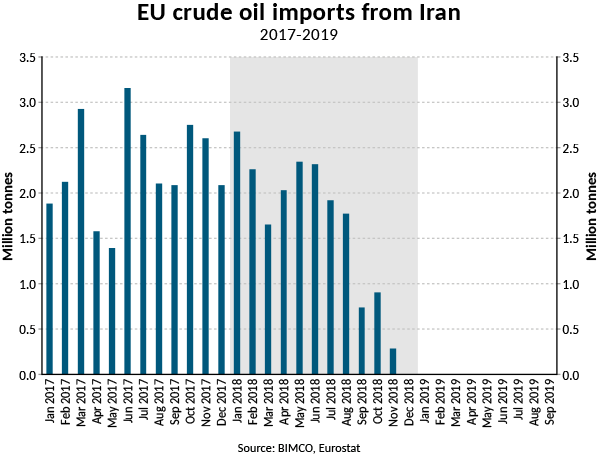

On a geopolitical level, tighter US sanctions on certain oil tankers and shipping companies – as well as those limiting crude exports from Iran and Venezuela – and tension in the Persian Gulf and Red Sea, all had a significant impact on the market.

The geopolitics was combined with the seasonal boost that Q4 traditionally brings to the tanker market and mixed with refiners which were desperate to get crude oil to their facilities to ramp up production ahead of the new sulphur cap, which is likely to be highly lucractive.

The geopolitics was combined with the seasonal boost that Q4 traditionally brings to the tanker market and mixed with refiners which were desperate to get crude oil to their facilities to ramp up production ahead of the new sulphur cap, which is likely to be highly lucractive.

Fleet news

In anticipation of a strong demand boost from the IMO 2020 Sulphur Cap, shipowners have pushed up fleet growth – higher than needed, if judged by freight rate developments.

The oil product tanker fleet has seen a sharp rise in deliveries from 2018 which, combined with lower demolition, means that BIMCO now expects fleet growth of 4.8% in 2019, compared with 1.8% in 2018.

The largest share of the additional capacity comes from deliveries of Medium Range (MR) tankers. These average 48,549 DWT in size, bringing an extra 4.1m DWT into the fleet in the form of 85 ships. The majority of the remaining delivered capacity comes from 24 new LR2 tankers, amounting to 2.6m DWT.

Outlook

The International Energy Agency (IEA) expects OPEC production to fall by 1mbp in 2020 to 29mbp. In its latest World Oil Outlook, OPEC forecasts that, although its output will continue to fall through to 2024, worldwide oil supply is expected to rise. OPEC predicts 60% of global oil supply growth during this period will come from the US.

For shipping, the increasing proportion of exports from the US brings a higher tonne per mile demand as the US boasts longer sailing distances to European and Asian importing countries than many OPEC nations. This is one of the reasons why sanctions on Iran may give a boost to the tanker shipping industry. Increased US exports, including those to Asia, come despite a sharp drop in exports to China in the second half of 2018 and 2019 as a result of the trade war.

Anecdotal evidence suggests that a considerable number of VLCCs are being used as floating storage, especially in the Far East, ahead of the IMO 2020 sulphur cap added to which, ships are being taken out of the market for scrubber retrofits. Both of these developments have reduced the available capacity, supporting already high freight rates. This is however, a short term gain, as when these ships return to the market, the boost to freight rates will be gone.

BIMCO still expects the IMO 2020 Sulphur Cap to bring a boost to oil product tankers and help keep rates profitable in Q4 2019 and the first few months of the new year. Although the tanker shipping industry is likely to be the only part of the sector to see increased demand from the stricter sulphur cap, it will also face the same additional costs associated with compliance as other shipping segments.

__

Much more here: https://www.bimco.org/news-and-trends/market-analysis

Looking for Training: https://www.bimco.org/training/courses/2019/1128_market-insights-seminar_bimco-house

IMO2020 Bunker price news:

https://www.bimco.org/news/market_analysis/2019/20191107_imo2020_market_uncertainty

https://www.bimco.org/news/market_analysis/2019/20191107_fuel_spread_32_ports

About BIMCO: https://www.bimco.org/about-us-and-our-members