BIMCO: Chinese imports heading for 50% market share of the dry bulk market after a turbulent year

The turbulence of the past year has in many ways clouded the underlying fundamentals in the dry bulk

shipping market, but with 2020 now behind us, we are in a better position to establish an overview of

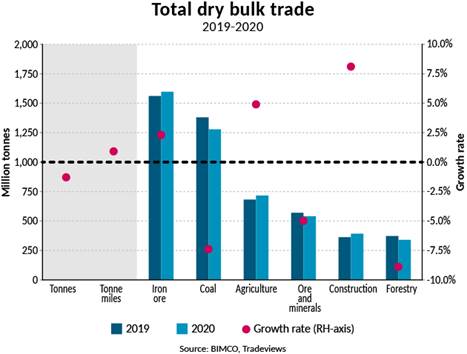

expectations for 2021. Overall, total tonnes transported by the dry bulk shipping industry fell by 1.3% to 5.49 billion tonnes, from 5.56b in 2019, which is however still higher than the 5.46b tonnes shipped in 2018. China has further cemented its position as the dominant player in dry bulk shipping with its imports now accounting for just shy of 50% of the market when measured in tonne-miles.

This overall drop in tonnes marks discrepencies between different dry bulk commodities. Of the three main commodity grous: iron ore, coal and agriculture, coal is the only one to have fallen; down 102.2 million tonnes from last year (-7.4%).

Iron ore and agricultural goods have, on the other hand, risen in 2020, up by 36.9m tonnes (+2.3%) and

33.3m tonnes (+4.9%) respectively, cementing iron ore’s position as the highest volume dry bulk good. In

percentage terms, the biggest growth has come from construction, which grew by 8.1% in 2020, but as

absolute volumes are much lower, this translated into an extra 29.6m tonnes. The largest commodity in the

construction category is cement, which saw a 13.4% increase between 2019 and 2020. China accounted for

half of this 21.5m tonne increase, as the country sawits seaborne cement imports rise by 52.2% (12.7m

tonnes).

At the other end of the scale, the largest percentage drop came from foresty, down 8.9%, or 33.0m tonnes.

Half of this drop comes from wood in rough, down by 14.9 million tonnes (-17.4%). 10.6m tonnes of the

14.9m loss came from lower imports into China.

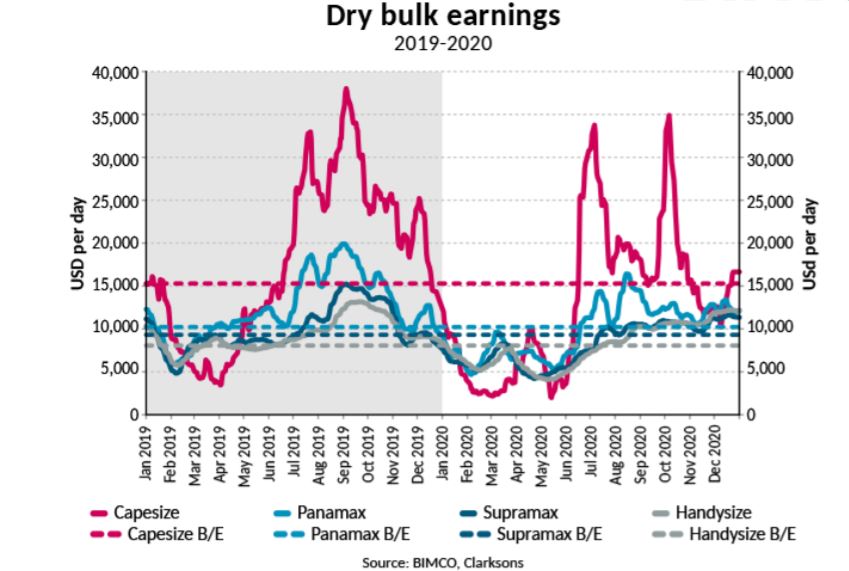

”For dry bulk shipping, the year can be divided in two, with lower volumes and earnings in the first half

followed by a recovery in the second, as China split from the rest of the world, boosting tonne and tonne

mile demand, and sending freight rates to profitable levels. June was the turning point as volumes reached

their highest point of the year, and earnings jumped, especially for Capesize ships,” says Peter Sand,

BIMCO’s Chief Shipping Analyst.

Chinese imports now account for 48.5% of the market, leading to year-on-year growth in tonne miles

In many ways following the narrative of the year, there is a split between China and the rest of the world.

Splitting up the two in terms of dry bulk trade, China grew strongly last year, with volumes rising by 95.3m

tonnes (+5.2%). Amongst other things, Chinese imports of iron ore and soya beans have risen by 7.1% and

12.0% respectively.

The strong growth in Chinese imports has however not been enough to make up for the fall in imports by

the rest of the world when measured in tonnes. Here, demand fell by 4.5%, amounting to 167.7m tonnes,

overshadowing the growth in China.

On average, imports to China sailed 1.8 times further than those to the rest of the world. These longer

distances meant that when measured in tonne miles rather than tonnes, growth in China was more than

enough to make up for the fall in the rest of the world. Tonne mile demand to the rest of the world fell by

6.2% and with China’s rising by 9.6%, total growth came to 0.9%.

The increase in Chinese imports means that the tonne mile demand from these accounted for 48.5% of

total dry bulk tonne miles in 2020, up from 44.7% in 2019. In comparison, when measured in tonnes,

China’s share has risen from 32.8% in 2019 to 34.9% om 2020.

Tonne mile growth was a buffer for earnings

Across the board, dry bulk earnings averaged below breakeven levels in 2020, though no sectors

experienced average earnings below 2016 levels. Capesizes and Supramaxes were the hardest hit,

averaging daily spot market losses of USD 2,271 and USD 1,170 throughout 2020, while Panamax and

Handyssize ships were just a few hundred dollars below breakeven levels estimated by BIMCO.

Timing had a crucial role in determing owners’ profitablity, as rates in the second half of the year were

much better than those in the first, as the recovery in China helped lift the dry bulk market.

The slight growth in tonne mile demand did little to offset the 3.8% fleet growth in 2020, or 33.3 million

DWT, thereby adding 2020 to the growing list of years which experienced a deterioration in the

fundamental market balance.

Heading for a record breaking year

With 2021 now upon us, the obvious question is where is the world going now and how will it impact the

dry bulk shipping industry? BIMCO expects China to continue to increase its dominance, though growth is

likely to be more focused on private consumption rather than the infrastructure heavy stimulus measures

of last year, somewhat dampening dry bulk imports.

As the rest of the world starts on its slow and uneven path to recovery, the dry bulk industry will continue

to face challenges this year, demand will grow unevenly across the four dry bulk sectors, and fuel prices are

rising, adding pressure to earnings. Countering this, fleet growth is expected to be at its lowest level since

the turn of the century.

”We expect 2021 to be a record breaking year for the dry bulk industry both in terms of tonnes and tonne

miles, with demand growth likley outpacing that of supply. However, this will not solve the overcapacity

issue that has long plagued the dry bulk market and is an obstacle that will not disappear just because a

new year has started or a vaccine has been found,” says Peter Sand.