Dear Readers,

It is our pleasure to present the Q1 2026 edition of our Shipping Market Analysis Report. If the close of last year established a “new normal” of geopolitical sensitivity, the first quarter of 2026 has profoundly tested the maritime industry’s resilience against continuous, severe disruptions and unprecedented market volatility.

This quarter has been defined by a stark contrast: operators have had to manage immediate, acute geopolitical crises while simultaneously accelerating long-term, multi-billion-dollar commitments to decarbonization and fleet renewal. Across all sectors, the industry navigated a highly complex landscape. The Tanker and LNG/LPG markets faced immense supply shocks and route diversions—most notably due to escalating tensions in the Red Sea, the physical blockade of the Strait of Hormuz, and shifting sanctions in the Americas. These pressures kept vessel demand exceptionally high, drove freight rates up, and brought demolition activity to a virtual standstill as older tonnage remained vital for energy security.

Meanwhile, the Dry Bulk and Container sectors demonstrated remarkable adaptability. Despite facing the pressures of massive newbuilding deliveries, fluctuating industrial demand, and the necessity of rerouting voyages via the Cape of Good Hope, these markets remained robust, supported by strong second-hand asset plays and shifting global trade routes.

Yet, beyond the immediate freight fluctuations, the defining narrative of Q1 2026 is strategic foresight. The industry is aggressively transitioning from short-term reactions to “lifecycle optimization.” We are witnessing a historic surge in newbuilding orders focused strictly on dual-fuel capabilities, the rapid maturation of zero-carbon alternative fuels like ammonia and green methanol, and the scalable integration of wind-assisted propulsion and AI-driven navigation.

As the maritime landscape grows increasingly complex, we remain committed to providing the maritime community with timely and actionable insights. We encourage you to visit our dedicated platform, https://shippinganalytics.pms.uoa.gr/, which serves as a continuous extension of these quarterly reports, offering in-depth analysis of these transforming markets.

We hope you find this Q1 2026 analysis both insightful and valuable for navigating the turbulent, yet progressively green, waters ahead.

Warm regards, Dr. Michael Tsatsaronis Asst.Professor Dept. of Port Management and Shipping

National and Kapodistrian University of Athens

Editor – Head of Scientific Research:

Dr. Michael Tsatsaronis

Editorial Coordinators:

Dimopoulos Argyris, Gkorila Martha, Katsavos George, Markopoulioti Panagiota

Research Team:

Tankers Team: Mania Amalia, Vasileiadou Savvina, Kalli Aggelina, Pruidze Lazaros

Dry Bulk Team: Doumani Panagiota, Kaliakouda Nansy, Koutoufari Harista, Kardara Anastasia

Containers Team: Zacharopoulou Efthimia, Vitzilaiou Anastasia, Skouli Maria Aikaterini, Foteinakis Nikolaos

LNG/LPG Team: Karasavvidis Theocharis, Spyraki Sofia, Psihogiou Eleftheria, Boziotis Panagiotis

Sustainability Team: Polonyfi Stavriani, Karapanagou Aggeliki, Vounanioti Penny, Diamanti Elena

All graphs and tables are authors’ elaboration based on data from Clarksons’ Shipping Intelligence. For inquiries or cooperation, please contact: mtsatsaronis@pms.uoa.gr

Stay Connected:

TABLE OF CONTENTS

NEWBUILDING – SALES & PURCHASE 5

NEWBUILDING – SALES & PURCHASE 8

NEWBUILDING – SALES & PURCHASE 11

NEWBUILDING – SALES & PURCHASE 15

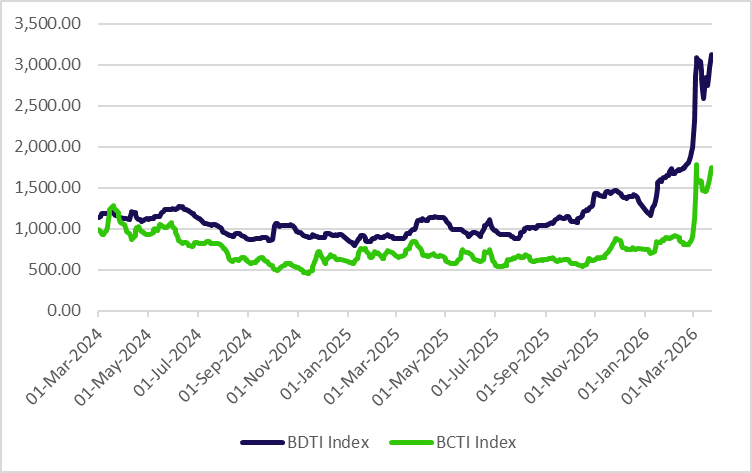

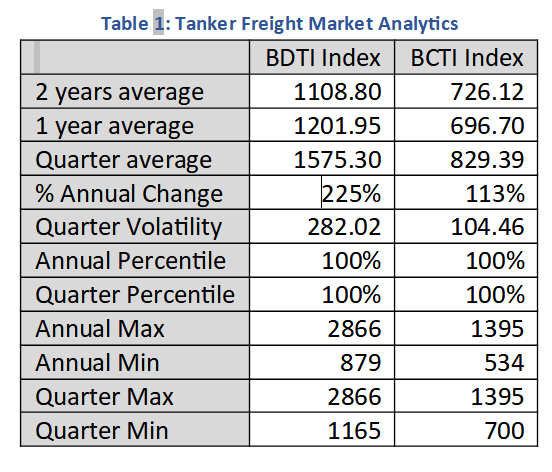

TANKER MARKET

In the first quarter of 2026, the tanker shipping market demonstrated strong positive momentum. The sector’s performance was primarily driven by robust demand for long-haul voyages, constrained vessel supply, and continuous geopolitical uncertainty. Throughout the quarter, the market navigated various international developments, shifts in global oil flows, and regional disparities in the recycling sector, ultimately resulting in a highly profitable.

FREIGHT MARKET

The freight market experienced significant fluctuations and realignments in Q1 2026. Early in the year, the oil tanker market began to recover from the lows recorded in early January. Freight rates for Very Large Crude Carriers (VLCCs), Suezmax, and Aframax vessels saw upward trends, largely due to the adjustment of global oil flows and the tightness of the available fleet.

Significant geopolitical developments heavily shaped the market’s trajectory. In Venezuela, political and social instability created new uncertainties regarding tanker fleet expansion. The country’s oil exports faced stringent U.S. sanctions and enforcement measures, which reduced available export capacity and elevated operational risks for vessels operating in the region. Furthermore, following changes in political leadership and military actions, the U.S. proceeded to seize tankers, leading the Venezuelan government to agree to supply American authorities with a substantial volume of oil. Despite a naval blockade, the United States intended to release oil production into the market and simultaneously grant special licenses to traders and companies for imports and exports.

Simultaneously, Canada significantly increased its oil exports via tankers, utilizing main loading ports such as Vancouver, Whiffen Head, and Point Tupper. These exports, predominantly carried out by Aframax and Suezmax vessels, were mainly directed to the U.S., though increasing volumes heading to Asia and Europe began altering the landscape of global oil flows.

By February, the tanker market remained strong but was characterized by high volatility, with geopolitics acting as the primary driver of developments. Freight rates were supported not only by underlying demand but also by supply chain disruptions and shifting trade routes. Sanctions on Russian oil contributed to the creation of a large “shadow fleet” and redirected European exports to Asia, which increased voyage distances and overall tanker demand. Concurrently, rising tensions in critical maritime chokepoints like the Strait of Hormuz, alongside attacks on vessels in the Black Sea and Red Sea regions, resulted in elevated risks, insurance costs, and freight rates.

Moving into March, the freight market exhibited signs of stabilization following the earlier volatility. Strengthened demand for crude oil transportation, particularly from the Arabian Gulf to major importers such as China, bolstered freight rates for VLCC and Suezmax vessels. The market tightened further due to limited vessel availability, which was exacerbated by fleet consolidation, cautious routing away from high-risk areas, and reduced traffic, pushing spot rates higher. Despite the ongoing risks of oil flow disruptions, routes through the Strait of Hormuz remained highly profitable for operators who navigated these challenges, as they benefited from elevated risk premiums. Increased activity and limited available capacity were also noted for LR2 and LR1 vessels during the quarter.

NEWBUILDING – SALES & PURCHASE

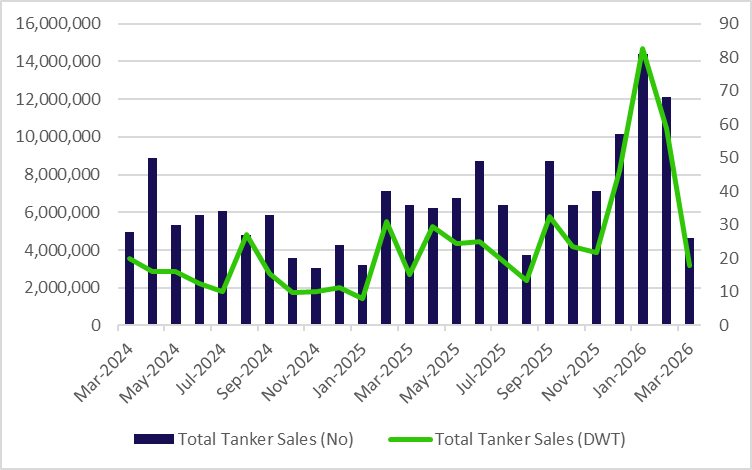

The first quarter of 2026 witnessed a resurgence of investment activity in tanker newbuildings, particularly for VLCCs, Suezmaxes, and modern product tankers, aimed at fleet renewal and expansion. Shipowners adopted a strategy centered on lifecycle optimization, making investment decisions based on efficiency, cost-effectiveness, and regulatory compliance. Consequently, investments were highly selective and focused on technologically efficient vessels with environmentally friendly characteristics, rather than pursuing massive fleet expansions.

Graph 2: Tanker Newbuilding Contracts

In February, a gradual increase in newbuilding activity was recorded, reflecting improved owner confidence. The overall orderbook remained at manageable levels compared to the active fleet, which alleviated immediate concerns about oversupply. Limited shipyard capacity and the growing demand for modern vessels constrained the pace of expansion and supported higher newbuilding prices. New orders, notably from Greek shipowners, were primarily directed toward shipyards in China and South Korea, with delivery windows extending from 2027 to 2032.

The second-hand (S&P) market also experienced robust activity throughout the quarter. Modern tanker units frequently changed hands, as investors leveraged resale opportunities alongside newbuilding contracts. In March, surging demand and rising freight rates for VLCCs drove second-hand vessel prices higher. Owners increasingly favored acquisitions of used ships over newbuildings, as the latter remained subdued due to high costs and significant shipyard delays. Furthermore, the strong chartering market, characterized by high spot and time charter rates, discouraged ship scrapping, keeping even older vessels in active operation. There was also a broader market shift of investment capital moving away from containerships and toward the tanker sector.

DEMOLITIONS

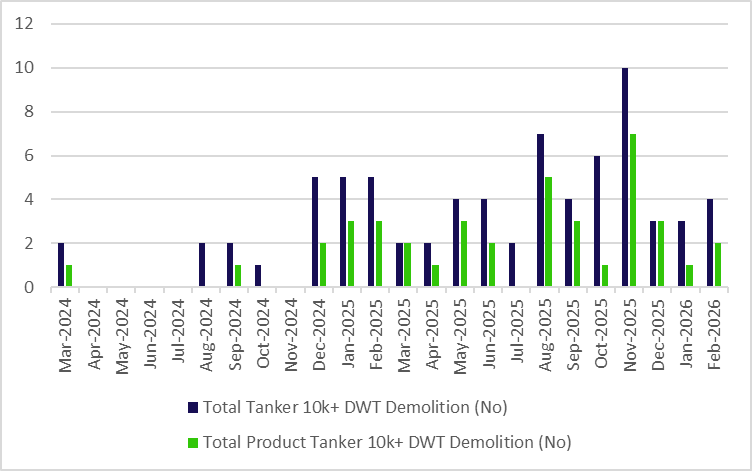

The tanker recycling and demolition market experienced varying conditions across regions during Q1 2026, largely supported by a persistent scarcity of available tonnage.

In January, the market began with weak to subdued conditions but gradually stabilized and strengthened as buyer confidence improved. Bangladesh consistently offered the highest price levels, reaching approximately USD 415 per LDT, maintaining its status as the premium destination. Conversely, the Indian market faced depreciation pressure on the rupee, while Pakistan saw limited buyer presence due to an inability to compete with pricing in India and Bangladesh. Turkey’s imports softened with minimal local market movement.

February saw firmer conditions, with intensified competition for the extremely limited supply of suitable recycling candidates. Bangladesh continued to command the highest prices, peaking at USD 430 per LDT, with buyers maintaining aggressive interest, though yard capacities were reportedly filling up. India remained a workable destination and participated actively despite currency volatility, although tighter measures were implemented for sanctioned vessels. Pakistan’s buying activity was selective, focusing on HKC-approved yards, while the Turkish market remained steady.

By March, regional disparities became more pronounced. Bangladesh sustained healthy demand and firmer pricing levels as buyers sought to acquire the limited available tonnage. In contrast, the Indian market slowed down significantly due to a strict approach from the Directorate General (DG) of Shipping regarding sanctioned vessels and disruptions in the supply of natural gas. Pakistan’s market remained unchanged, with participants adopting a wait-and-watch approach amid ongoing geopolitical tensions. Ultimately, macroeconomic uncertainties and geopolitical conflicts weighed on the sector, but the market remained supported overall by the constrained supply of vessels.

DRY BULK MARKET

The first quarter of 2026 for the dry bulk market has been characterized by a combination of strong trading volumes, dynamic shifts in commodity demands, and a highly active second-hand vessel market. Despite structural economic changes and geopolitical disruptions, the sector demonstrated resilience and adaptability, supported by increasing ton-mile demand and strategic investments by shipowners.

FREIGHT MARKET

The dry bulk freight market exhibited robust performance and notable volatility throughout Q1 2026, driven by shifting global trade patterns. Closing out 2025 and entering January 2026, international seaborne trade volumes reached a new historical record, exceeding 5.7 billion tonnes, which represented a 1.7% increase compared to 2024. This momentum carried into early 2026, with the Baltic Dry Index (BDI) recording a 6% to 7% increase toward the end of January, buoyed by strong trading volumes. By February, the Baltic 5TC and 7TC indices indicated a broad recovery across all vessel segments, with freight rates experiencing notable volatility alongside an overall upward trend. Vessel transits through the Suez Canal during the first week of 2026 remained low, standing at 60% compared to 2023 levels.

Demand varied significantly across vessel classes. Capesizes benefited from a 30.8% increase in bauxite production, driving specific demand for this raw material and leading to a 1.8% growth for the segment in early 2026. Meanwhile, Supramaxes and Handysizes saw a 3.4% growth, largely benefiting from grain exports originating from the East Coast and South America. The Supra/Ultramax category recorded the most substantial growth at 4.7%.

In February, ton-miles increased by up to 2.5%, largely due to ships hauling iron ore and bauxite on long-haul routes from the South Atlantic (Brazil and Africa) to Asia. The Guinea-to-China bauxite route, which saw an 18% volume spike in 2025, heavily contributed to this demand. Massive Capesizes and Very Large Ore Carriers (VLOCs) capitalized on these long-haul routes, achieving rates of nearly $25,000 a day. Furthermore, a surge in “green” minerals, such as lithium-bearing ores for electric vehicle batteries, provided a significant boost to smaller ships like Handysizes and Panamaxes.

In March, geopolitical tensions impacted operations, with conflict situations in Asia trapping 236 bulk carriers in the Persian Gulf as of March 13th. Despite this, the safety of the crews was not compromised, and the general bulk carrier market and global exports were not significantly affected. Coal exports, however, reflected a global transition toward cleaner energy sources, decreasing year-on-year in 2025 partly due to new political formulations in Indonesia.

DRY BULK

Panamax and Post-Panamax vessels handled the bulk of these exports, transporting 822 million metric tons in 2025, a figure predicted to reach 825 million by the end of 2026. Looking ahead, Veson Nautical predicts uncertainty for the remainder of 2026 due to structural changes in China’s economy and ongoing decarbonization efforts. Nevertheless, the agency still anticipates a 2.5% market increase by the end of the year, supported by green energy infrastructure investments, favorable interest rates, and the expansion of the Guinea-to-China trade route.

NEWBUILDING – SALES & PURCHASE

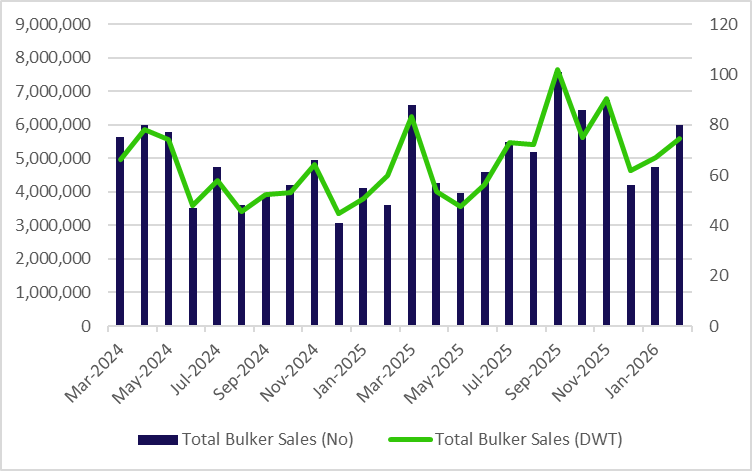

The Sale and Purchase (S&P) market experienced an unusually strong start to the year. Typically quiet in the first few months, early 2026 saw intense transaction activity. Between January 1st and February 20th, 109 bulk carriers were sold, representing a 36% year-on-year increase compared to the 80 ships sold during the same period in 2025. This diverse second-hand market was primarily driven by Supramax and Handysize vessels, with 23 sales each. This was followed by Ultramaxes with 19 sales, Capesizes with 16 sales, Kamsarmaxes with 15 sales, and Panamaxes with only 5 sales. Vessel prices remained stable, with older Handysize vessels demonstrating particular resilience and strength in the market.

Conversely, the newbuilding market showed a notable contraction in total volumes early in 2026, with overall orders dropping by 49%, bringing the active orderbook to 325 new vessels. The Post-Panamax category saw the steepest decline at 79%, while Capesize orders saw the smallest drop at 17%. Despite the overall drop, strategic fleet investments continued strongly. January saw the successful delivery of the world’s first methanol dual-fuel Kamsarmax, named the “Brave Pioneer”, by Tsuneishi Heavy Industries Inc. Prominent Greek shipowner Evangelos Marinakis (Capital Maritime) signed a $540 million contract in China covering two VLCCs and four Capesize bulk carriers. Additionally, Yangzijiang Maritime Development ordered six firm vessels with options for ten more, and Danaos entered the bulker newbuilding market for the first time with a six-ship order program. In February, newbuilding interest was mainly focused on the Kamsarmax segment due to its commercial flexibility. By January 2026, the global bulk carrier fleet consisted of 13,120 ships, and it is expected that 438 new orders will be delivered by the end of the year.

DEMOLITIONS

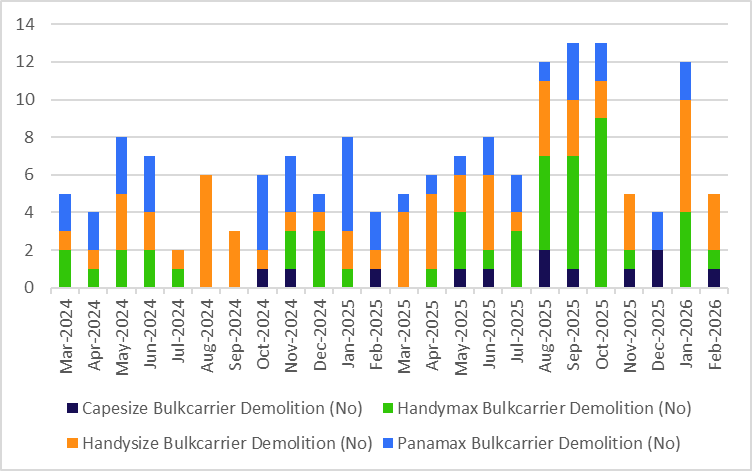

The demolition and recycling market for the dry bulk sector remained sluggish throughout the first quarter of 2026. Activity consistently hovered at low levels, well below the historical average. The primary driver for this slow pace was the robust freight market and the highly active second-hand vessel market, which provided shipowners with sufficient returns to justify keeping older vessels in active operation rather than sending them to scrapyards.

Shipowners consistently preferred to either continue operating their aging bulkers or sell them to other buyers for further trading. As a result, the few recycling deals that were reported mostly involved exceedingly old vessels that were no longer economically efficient to run. Furthermore, the recycling market was negatively influenced by external macroeconomic factors, including reduced steel prices and currency fluctuations in key ship-breaking destinations such as India, Bangladesh, Pakistan, and Turkey. Looking forward, BIMCO estimates that the demolition market for bulk carriers will remain subdued for the entirety of 2026, with an estimated total of only 2.8 million dwt expected to be scrapped.

CONTAINER MARKET

The first quarter of 2026 presented a highly dynamic and fluctuating environment for the global containership market. The quarter commenced in January on a relatively positive and stable footing, supported by constrained capacity and high fleet utilization. However, the landscape quickly shifted into a downward trend during February, heavily influenced by traditional seasonal lulls associated with the Chinese New Year and a corresponding reduction in industrial activity. By March, the market was engulfed in heightened uncertainty due to escalating geopolitical tensions in the Middle East, maritime transport disruptions, and rising energy costs, resulting in a notably cautious medium-term outlook. Despite the volatility in the freight market, shipowners continued to strategically invest in fleet renewal, prioritizing environmentally compliant, dual-fuel newbuildings to adapt to shifting trade routes and future disruptions. Meanwhile, the demolition sector, which began the year in a stagnant state, slowly awakened as the quarter progressed, driven by the pressure of massive newbuilding deliveries and the looming enforcement of stricter carbon standards.

FREIGHT MARKET

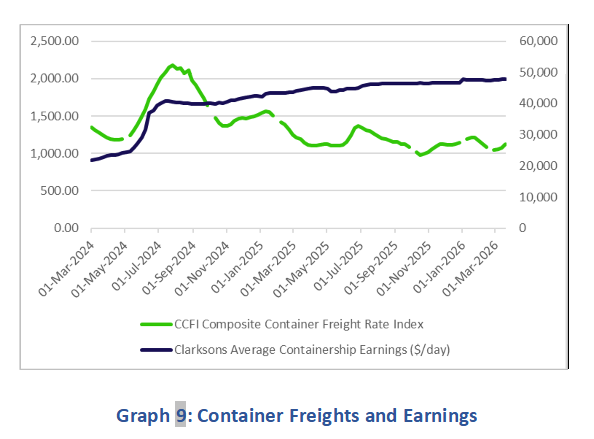

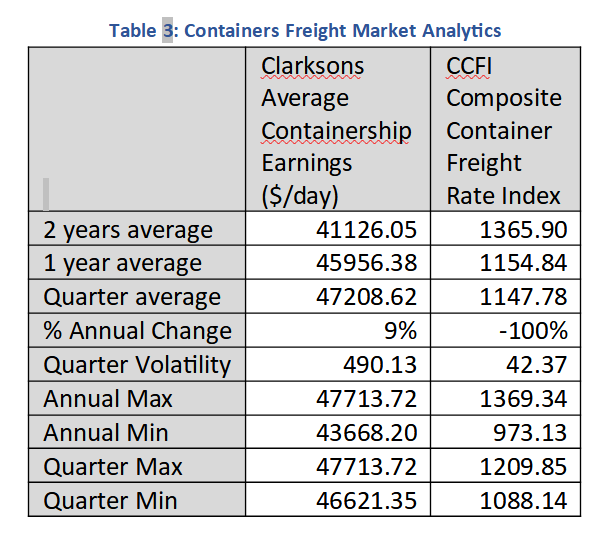

The containership freight market experienced significant volatility and varying pressures throughout the first quarter. During January, the market demonstrated clear signs of measured strengthening. The broader conditions remained highly supportive of operators, even though there was an absence of a clear and unified market direction. Freight rates were successfully maintained at stable levels, an achievement directly attributed to high fleet utilization and notably limited levels of idling. Furthermore, constrained capacity availability across certain vessel sizes acted as a crucial stabilizing factor. Despite these positive indicators, market performance was not uniform across all trade lanes, with noticeable variations observed in fundamental demand dynamics and charter duration lengths. Within this complex environment, market participants kept their activity highly selective, focusing intensely on risk management and the preservation of operational flexibility. Overall, January reflected a market operating on a positive footing but plagued by limited visibility, with rates influenced simultaneously by supportive fundamentals and ongoing macroeconomic uncertainties.

Transitioning into February, the containership freight market experienced a distinct downward trend. Weekly data consistently indicated successive declines in overall freight rates. This negative development was primarily associated with fundamentally weaker demand during the period surrounding the Chinese New Year holidays. During this time, industrial and manufacturing activity in China was temporarily reduced, severely impacting export volumes. Consequently, the market presented a significantly more subdued outlook. The underlying demand for maritime transport appeared visibly lower, directly causing freight rates to move and settle at reduced levels.

By March, the narrative of the freight market was completely characterized by increased global uncertainty. The market operated under the heavy impact of intense developments and conflicts in the Middle East. Reduced capacity availability became a prominent issue due to severe disruptions in global maritime transport, which subsequently created immense operational pressures on the market. Furthermore, rising energy costs began to negatively affect the broader economic environment. Concurrently, weaker global demand paired with lower expected growth in overall container trade contributed to a much more cautious market outlook. Because of these combined negative factors, the market’s prospects remained highly uncertain in the medium term.

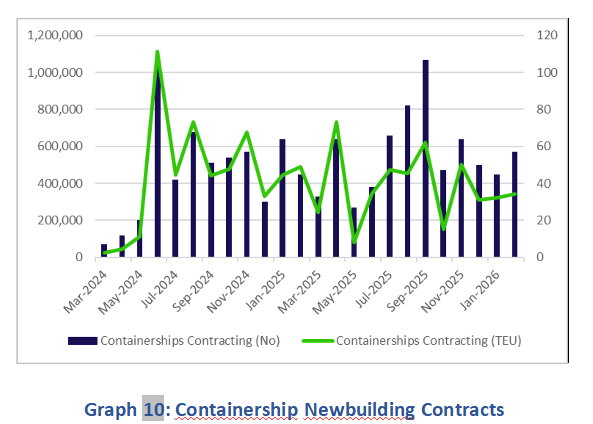

changes in global shipping routes. The market was fully expected to continue at this exact same aggressive pace into 2026. This projection proved accurate in January, which recorded fresh orders for a total of 16 new ships, while the prominent operator Evergreen notably ordered 23 new vessels directly from a Chinese shipyard. Despite the industry facing a huge number of TEUs scheduled to be delivered within the year, shipping companies actively continued to invest heavily in shipbuilding to effectively cope with future geopolitical and economic disruptions.

In February, overall ordering activity continued, albeit at a noticeably slower pace compared to the previous month. A major highlight was Maersk placing a significant order for eight large dual-fuel containerships, a move that heavily reinforced the industry’s strategic shift toward strict environmental regulatory compliance. In parallel, market reports strongly highlighted that the recent massive surge in containership orders had successfully led to historically high TEU levels within the global orderbook. Furthermore, the average size of vessels specifically scheduled to operate on the major East-West routes continued to aggressively increase, accurately reflecting the ongoing and dominant trend toward deploying significantly larger ships.

March was heavily marked by escalating geopolitical tensions in the Middle East, a situation that created even greater uncertainty for the shipping market. Nevertheless, new containership orders bravely continued. The indefinite avoidance of the critical Strait of Hormuz by major shipping companies is fully expected to absorb any excess fleet capacity due to the necessity of rerouted, significantly longer voyages traveling via the Cape of Good Hope. During this tense period, Euroseas Ltd. specifically ordered two new, highly specialized 2,800 TEU high-reefer containerships from the Huanghai Shipbuilding Co., Ltd. shipyards located in China. Additionally, Yang Ming successfully ordered six newbuilding containerships, each boasting a massive carrying capacity of 13,000 TEU. These specific newly ordered ships will feature advanced dual-fuel and LNG capabilities. Analysts project that significantly more orders will be finalized and announced by major companies in the upcoming few months.

The Sale and Purchase (S&P) sector for containerships exhibited varied momentum. The year commenced with strong indicators in January, reflecting a rising demand for containerships. BF Shipmanagement completed the purchase of a 2023-built Neo-Panamax vessel, boasting a capacity of around 13,000 TEU, from its previous owner, Capital Clean Energy Carriers (CCEC). Furthermore, the Tsakos Group successfully acquired a second-hand Panamax vessel, featuring a capacity of approximately 4,500 TEU and built in 2010, from Atlantica Shipping. These high-profile purchases successfully indicated a strong start for the second-hand containership market in 2026.

Activity persisted into February, albeit on a slightly smaller scale, when Metrostar Management Corp officially acquired the vessel named Warnow Beluga. This specific vessel is a feeder ship that was originally built in 2008 and holds a total capacity of 1,300 TEU.

By March, however, there was a recorded low level of activity across the Sales & Purchase containership market. According to market sources, MSC purchased two Sub Panamax vessels. Both of these acquired units were built in 2006, feature a capacity of 2,602 TEU, and cost the operator 25 Million USD each. Additionally, during this slow month, the vessel known as “Erasmus Oasis” was officially sold for 11 million USD to an undisclosed, unknown buyer. This specific vessel operates as a feedermax ship and has a listed capacity of 1,049 TEU.

DEMOLITIONS

CONTAINERS

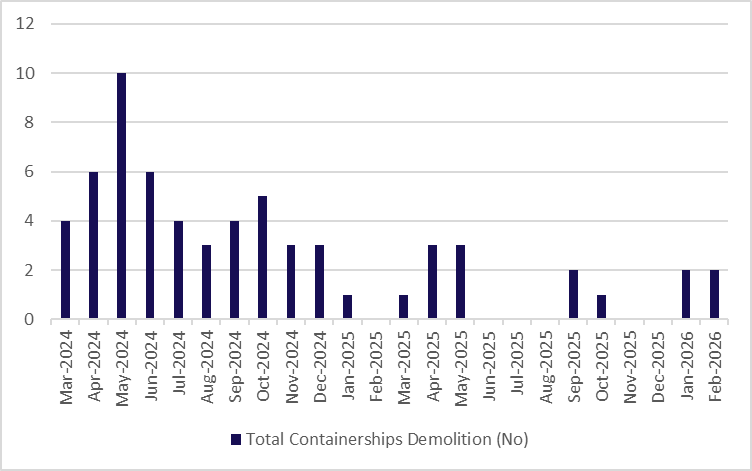

Demolition of containerships has dropped globally to historic lows in 2025: only eight to ten containerships have been scrapped so far this year, compared with 81–82 units in 2023. Simultaneously, BIMCO estimates that at least 500 containerships (≈ 1.8 million TEU) globally are overdue for recycling—the highest backlog since the 1970s. By 2025 a quarter of the global containership fleet exceeds 20 years old. Such a sharp drop in containership scrapping despite an aging fleet and record backlog suggests that many older ships will remain in service for the foreseeable future. Unless demolitions rise dramatically in 2026, the overhang of obsolete capacity risks contributing to oversupply, downward pressure on freight rates, and idle tonnage in the medium term, leading to serious market imbalance within 2027.

Graph 12: Recycling Market Price

The market finally showed promising signs of awakening during February. Several aging units, most notably including the feeder vessel “Sunny Spruce”, finally withdrew from the active fleet for permanent recycling. Completely overlooking the currently high charter rates, the undeniable mounting pressure of incoming newbuilding deliveries slowly but steadily began forcing older tonnage out of active service. Industry analysts firmly expect scrap prices to remain strong and firm at approximately $510/LDT, a price level heavily supported by an increasingly tightening supply of viable ships.

March subsequently witnessed a slight but notable uptick in ship recycling activity. Owners practically began offloading vintage maritime units, such as the vessel Kokopo Chief, as a strategic maneuver to carefully manage comprehensive fleet renewal. While the broader demolition market remains incredibly tight due to persistent ongoing regional disruptions, scrap prices successfully stabilized at highly attractive financial levels. During March, these prices currently averaged $465/LDT within the shipyards of Bangladesh. Expert industry sources strongly suggest that the potent combination of a massive global orderbook and the implementation of much stricter carbon emission standards will inevitably drive significantly more mid-sized tonnage directly toward the breakers by the end of the current year.

LNG/LPG MARKET

The first quarter of 2026 proved to be an exceptionally dynamic and historically significant period for both the Liquefied Natural Gas (LNG) and Liquefied Petroleum Gas (LPG) shipping markets. The quarter began with a stabilizing seasonal softness, where market fundamentals remained broadly supportive despite temporary drops in spot rates. However, as the quarter progressed, intense regional divergences emerged, ultimately culminating in severe market shocks driven by unprecedented geopolitical conflicts and infrastructure disruptions. Despite the intense volatility experienced in the freight markets, shipowners demonstrated immense confidence in the long-term viability of gas transport by executing a historic surge in newbuilding orders, pushing the global orderbook to record heights. Conversely, this urgent need for available maritime capacity in a constrained market environment brought vessel recycling and demolition activities to a complete standstill, as operators prioritized immediate fleet availability over the retirement of aging units.

FREIGHT MARKET

The freight market for gas carriers experienced a remarkable evolution throughout the first three months of the year, transitioning from managed stability to extreme volatility. In January 2026, the LNG freight sector experienced a highly notable uptick, effectively continuing the strong, resilient momentum that had previously prevailed throughout the entirety of 2025. However, activity within the immediate spot market remained relatively subdued. This was primarily attributed to unexpectedly mild winter conditions across key consumption regions in Europe and Asia, which drastically reduced the immediate pressure on nations and utility companies to aggressively replenish their natural gas inventories. Consequently, this lack of immediate demand, combined with notably narrower arbitrage margins between major global natural gas hubs, led to an overall increase in available vessel capacity. This excess availability subsequently pushed Time Charter Equivalent (TCE) levels lower across both the Atlantic and Pacific trading basins. Despite this temporary seasonal softness, the underlying structural foundation of the market remained incredibly strong. This resilience was heavily supported by the continued global expansion of LNG as a critical transition fuel for the future, alongside the stabilizing effect of long-term charter contracts that successfully tied up the vast majority of the global operating fleet.

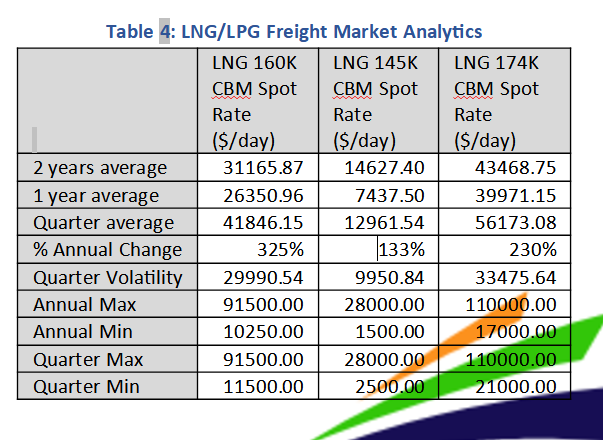

Moving into February, the freight market exhibited a marked and highly pronounced geographical divergence. Specifically, within the Atlantic basin, freight rates strengthened significantly. Modern MEGI and XDF vessels were successfully chartered at highly lucrative rates of around $35,000 per day, a surge driven by the continuous, unyielding European demand for U.S.-produced LNG cargoes. In stark contrast, the Pacific market fundamentally lagged behind, with spot earnings hovering at a comparatively lower $27,000 per day. Simultaneously, the LPG sector demonstrated exceptional strength. The market remained exceptionally robust, with average Very Large Gas Carrier (VLGC) TCE earnings rocketing to exceed $50,000 per day. This incredible profitability was directly driven by record-breaking U.S. Natural Gas Liquids (NGL) production and highly favorable arbitrage conditions directing flows toward Asian markets.

By March, the global situation changed dramatically and abruptly due to the eruption of serious geopolitical tensions. The physical blockade of the critical Strait of Hormuz acted as a massive catalyst, trapping exactly 47 LPG vessels and 20 LNG vessels, which caused an immediate and severe supply shock to the global fleet. Compounding this crisis, following targeted drone attacks on vital energy infrastructure in Qatar, QatarEnergy was forced to declare a state of force majeure, officially suspending operations at the massive North Field. These cascading disruptions sent energy prices soaring across Europe and kept spot charter rates in the Atlantic at extremely high, unprecedented levels. Charterers frantically scrambled to secure whatever vessels were available amid the mounting uncertainty and the rapidly increasing war risk insurance premiums.

NEWBUILDING – SALES & PURCHASE

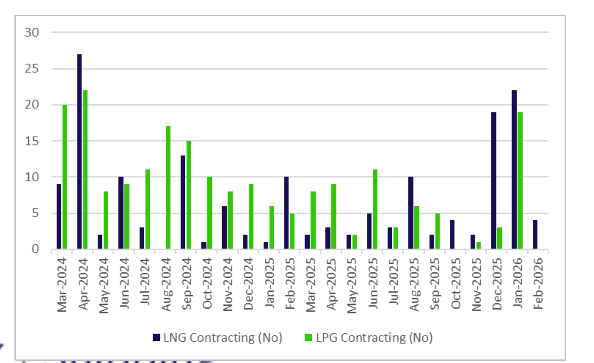

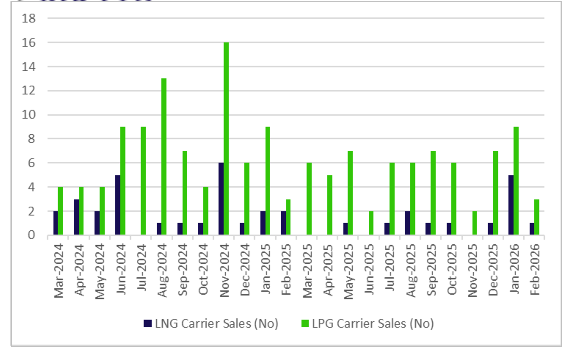

The first quarter of 2026 was undeniably marked by a historic, industry-defining surge in shipbuilding activity, which was particularly concentrated within the LNG sector. Shipowners aggressively positioned themselves for the future, heavily investing in the expansion and modernization of their respective fleets. In January, South Korean shipyards continued to exert absolute dominance over the market by securing massive orders that completely filled their forward delivery slots all the way through the year 2029. Notably, major strategic moves during this period included Alpha Gas placing firm orders for two new LNG carriers, while Capital Clean Energy officially ordered three massive 174,000 cubic meter (cbm) vessels directly from HD KSOE.

This aggressive ordering process drastically accelerated in February, with the broader market actively expecting over 100 new LNG carrier orders to be placed within the calendar year. Prominent Greek shipowners played a highly decisive and influential role in this expansion, effectively controlling a huge portion of the global orderbook, boasting an impressive 58 vessels under construction as of early 2026. Additional massive fleet expansions included TMS Cardiff Gas securing four new vessels at the Hudong-Zhonghua shipyards, while simultaneously, TEN began intense negotiations for a new, advanced series of 2+2 vessels at HD Hyundai. Meanwhile, within the LPG sector, Erasmus Shipinvest successfully took physical delivery of the specialized 5,000 cbm vessel known as “Gas Long”, which was immediately secured and chartered by energy giant Equinor.

By the end of March, the staggering scale of industry investment was evident, as the global LNG orderbook had officially exceeded an incredible 330 vessels. Capital Clean Energy Carriers Corp. stood out prominently as a market leader with 9 highly advanced LNG carriers actively under construction. Concurrently, the Vafeias Group strategically expanded its operational presence within the highly specialized LPG sector by acquiring 2 VCM carriers from the Sasaki shipyard.

In addition, Dorian LPG significantly strengthened its active fleet with the successful delivery of the advanced dual-fuel VLGC named “Areion”. This specific delivery perfectly reflected the overarching industry trend of heavily investing in modern, technologically advanced vessels that strictly comply with the International Maritime Organization’s (IMO) increasingly stringent environmental regulations.

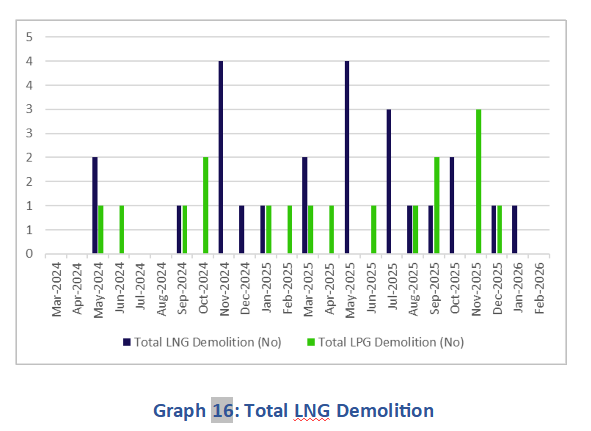

DEMOLITIONS

As directly requested, the analysis of the demolition sector remains concise, reflecting a period of profound stagnation. Scrapping activity remained virtually absent throughout the entirety of the first quarter of 2026. The exceptionally tight balance between available ship supply and intense global demand effectively prevented shipowners from scrapping their older, aging vessels. During January and February, even the industry’s least efficient, steam turbine-powered LNG carriers found continuous, highly profitable employment on regional routes or acting as floating storage units. Despite their notoriously higher fuel consumption and elevated emissions, these older vessels—which account for over 20% of the total global LNG fleet—remained highly economically viable.

In the LPG sector, incredibly strong vessel values and high VLGC earnings guaranteed that absolutely no significant vessels were sent to the scrapyards. By March, the escalating geopolitical crisis in the Middle East and ensuing disruptions in the Suez and Hormuz straits further constrained the global market, making every single available vessel utterly critical to global energy security. Consequently, shipowners exhibited a complete, unwavering reluctance to withdraw any operating vessels, definitively highlighting a market environment where the urgent need for immediate transport availability far outweighed any desires for fleet renewal through demolition.

SUSTAINABILITY

NEWS

During the first quarter of 2026, the maritime industry faced a landscape marked by regulatory uncertainty and accelerating decarbonization pressures. In response, shipowners shifted away from short-term decision-making, favoring resilient, long-term strategies centered on lifecycle optimization. This approach integrates environmental impact, operational efficiency, and economic performance across a vessel’s entire lifespan. Throughout the quarter, significant investments in alternative fuels, wind-assisted propulsion, and digital optimization demonstrated the sector’s commitment to reducing its carbon footprint. Simultaneously, the industry navigated geopolitical tensions and energy market volatility, highlighting the growing intersection of environmental, social, and governance (ESG) factors in shipping operations.

Regulatory Developments and Compliance Frameworks

Regulatory pressures intensified globally throughout Q1. Early in the year, ongoing discussions regarding the EU Emissions Trading System (ETS) emphasized the expanding influence of climate regulation on maritime investments and operations. Regulatory clarity also improved under the EU FuelEU Maritime framework for LNG carriers utilizing boil-off gas. Updated guidelines now allow for more accurate greenhouse gas calculations that incorporate methane slip and recognize lower-GHG fuels. However, debates continued at both the EU and IMO levels regarding the appropriate well-to-tank emission intensity factors for LNG.

In February, the International Maritime Organization (IMO) agreed on a draft work plan to establish comprehensive safety frameworks for ships using alternative technologies, including batteries, wind propulsion, and nuclear power. This plan outlines future SOLAS amendments to permit batteries to serve as a primary power source, alongside updates to the Nuclear Code. Furthermore, environmental regulations tightened geographically, with new Emission Control Areas (ECAs) established in the Canadian Arctic and the Norwegian Sea. These ECAs introduce stricter limits on sulphur oxides (SOx), nitrogen oxides (NOx), and particulate matter. Concurrently, South Korea took a leading role in developing international safety and marine discharge standards for ammonia-fueled vessels, preparing draft frameworks for submission to the IMO.

Alternative Fuels and Decarbonization Pathways

The adoption of alternative fuels accelerated massively, with over 1,100 dual-fuel container ships and vehicle carriers delivered or on order, representing an industry investment exceeding $150 billion. Flexible decarbonization pathways, including fuel-flexible engines, hybrid systems, and modular designs, became crucial to mitigate the risk of stranded assets.

- LNG and Methanol: LNG-fueled vessels maintained a dominant presence in the global orderbook, confirming their role as a primary transitional fuel. Methanol also achieved operational milestones; the Hong Kong Seaport Alliance successfully completed the first SIMOPS (simultaneous bunkering and ship loading/unloading) at the COSCO-HIT terminal, utilizing green methanol.

- Ammonia: Ammonia gained significant traction as a credible zero-carbon marine fuel. The world’s first comprehensive Type Approval Certification (TAT) and Factory Acceptance Testing (FAT) for a two-stroke ammonia-fueled marine engine was completed, marking a major technological leap from development to regulatory-validated application. Alfa Laval also completed the FAT for its FCM Ammonia fuel supply system, certified by the China Classification Society. Additionally, Hanwha Ocean successfully delivered its first Very Large Ammonia Carrier, while Pilbara Ports and Yara Pilbara collaborated to develop a low-carbon ammonia bunkering hub in Western Australia.

- Other Innovations: Hydrogen marine engine technology advanced toward industrial maturation in Japan. Furthermore, circular economy practices gained attention, highlighted by initiatives converting plastic waste from cruise ships into viable marine fuel.

Wind-Assisted Propulsion and Energy Efficiency

Wind-assisted propulsion systems transitioned from experimental concepts to realistic, scalable solutions for radically reducing emissions. The integration of technologies like WindWings delivered significant fuel and CO₂ savings. The tanker sector saw increased adoption of these systems, with eSAIL installations marking the beginning of broader fleet implementation. To commercialize rigid aerofoil technology for large commercial vessels, Alfa Laval and Wallenius Marine formed a joint venture under the AlfaWall Oceanbird brand. By March, Laskaridis Shipping signed a Joint Development Program with bound4blue and Bureau Veritas to evaluate the integration of eSAILs across its entire fleet.

Beyond wind power, the industry explored Onboard Carbon Capture and Storage (OCCS), with ports like Rotterdam investigating it as a practical decarbonization pathway for long-distance routes, though large-scale implementation still depends on clearer international regulations. Furthermore, efforts to reduce underwater radiated noise (URN) from ships were expanded, supported by technical guidance that integrates noise reduction with broader energy efficiency improvements.

Digitalization, Autonomous Navigation, and Social Governance Digital transformation acted as a primary enabler for ESG goals. Autonomous navigation moved toward large-scale commercial deployment, exemplified by Avikus installing AI-driven autonomous navigation systems on 40 HMM vessels. In the supply chain, WiseTech Global and Hapag-Lloyd launched a pilot program integrating real-time IoT data across a fleet of approximately two million “smart” containers. This digital precision optimizes chain synchronization, reducing unnecessary rerouting, delays, and energy-consuming options, which directly lowers the environmental footprint. Space-based IoT also advanced, with Greece’s Prisma Electronics demonstrating how its MICE-1 nanosatellite can enhance maritime safety, sustainability, and operational efficiency.

From a broader ESG perspective, the maritime sector actively promoted the social dimension by supporting ongoing initiatives for women in maritime. Concurrently, global shipping dynamics and supply chains were severely tested by geopolitical tensions and bunkering disruptions in the Middle East. These challenges heavily underscored the vital importance of operational resilience, energy security, and robust corporate governance in navigating modern market volatility.